The rising challenge of powering data centres

The boom in data centres in the UK is set to fuel a strong demand for energy. We recently forecast that total electricity demand from data centres in the UK could grow fivefold over the next five years.

Meeting these exponential energy demands presents a challenge and, in this blog post, we examine what makes data centre electricity demand unique and the possible energy supply solutions likely to meet this demand.

Data centre electricity demand is unique

Energy needs of data centres are defined by three specific aspects that makes them stand apart from other major electricity users. The first is continuous uptime: data centres operate 24/7 with an industry standard of “five-9s” reliability—99.999% uptime, equivalent to less than 5.3 minutes of downtime per year. This level of reliability requires access to a stable and highly reliable source of electricity.

Secondly, they have high IT power demands. While average data centres consume 5–10 MW of power, hyperscale facilities, which are increasingly common, can exceed 100 MW. Third is their high spatial concentration and energy intensity. Data centres consume 10–50 times more energy per square metre than a typical commercial office building and tend to cluster geographically, creating hotspots of very high electricity demand.

Implications for data centre siting

The distinctive profile of data centre electricity demand makes access to reliable, continuous power an essential prerequisite for a data centre. In practice, this means that grid connections, proximity to substations, and competitively priced electricity sit at the top of developers’ checklists.

At the same time, the sustainability and emissions commitments of leading tech firms are shaping data-centre investment decisions. Every firm we analysed—including Microsoft, Amazon (including AWS), Google, and Meta—has pledged to source 100% renewable or carbon-free electricity, with some already achieving this across large portions of their operations. As a result, developers are actively seeking locations that can deliver not just power, but clean power.

Energy considerations sit alongside a set of more traditional locational factors. Network connectivity remains critical, and for user-facing workloads, proximity to end users is essential for minimising latency—the delay between an action and the system’s response. Yet aligning energy access with user proximity is not straightforward. Urban areas offer clear advantages for latency-sensitive services, but they also tend to suffer from limited available land, constrained grid capacity, and higher energy costs.

By contrast, facilities designed for non-user-facing workloads—particularly compute-intensive AI model training—face fewer of these urban constraints. Their performance is not tied to user proximity, which allows developers to prioritise locations with abundant land, stronger grid availability, and lower electricity prices.

Case study: the challenge in the UK — high energy costs and grid constraints

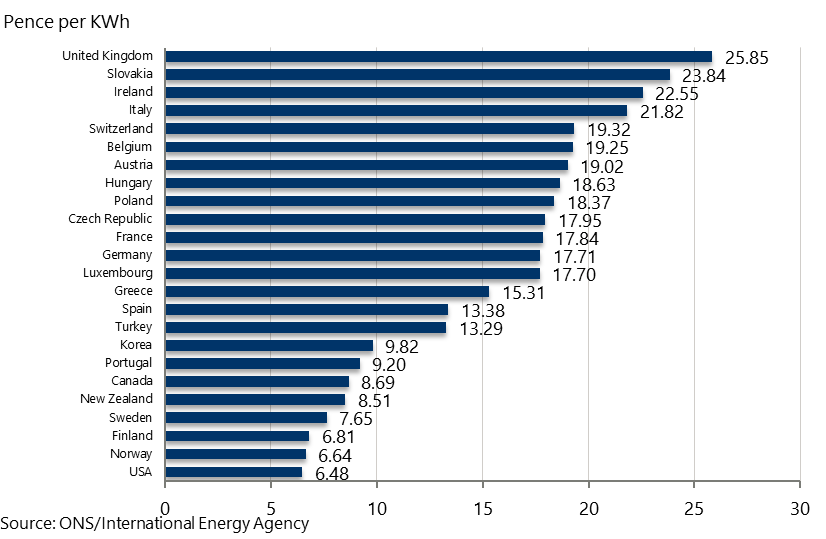

The UK has the highest industrial electricity prices among member countries (more than four times those of the US, Finland, Norway, and Sweden)—making it less competitive for energy-intensive AI training facilities that could otherwise be sited flexibly (Fig 1).

High electricity prices, and long waiting times hinder the attractiveness of the UK —data centre developers in the UK are currently waiting as long as 10 years for a grid connection.

Fig. 1. Industrial electricity prices by member country, 2023

Meeting the energy challenge: grid, behind-the-metre and hybrid generation

There are three ways to power a data centre—grid-tied, behind the metre, and hybrid.

The first is the traditional and dominant method that involves a standard connection to the national grid where power is purchased and delivered from the utility provider. It may face limitations related to grid capacity, leading to longer connection queues. Additionally, through a grid connection, data centres will take the generation mix on the grid, which may involve fossil-fuel powered electricity. Power Purchase Agreements (PPAs) offer a partial workaround. These long-term contracts allow data centres to buy electricity directly from specific renewable or nuclear generators, securing a cleaner supply and long-term price stability. Meta and Microsoft have signed large-scale PPAs for nuclear plants in the US. While PPAs still rely on physical grid connections—so they do not eliminate grid delays—they give operators the ability to match their consumption with low-carbon generation.

On-site generation involves power generated on site or adjacent to the data centre and connected directly to the customer—referred to as “behind the meter”. This model reduces exposure to grid connection delays and can ensure supply is generated by low-carbon sources. Electricity generation may be generated via Advanced Nuclear Technologies, such as Small Modular Reactors and Advanced Modular Reactors, or through renewable energy generation such as wind or solar plus storage backup or diesel generators to offset shortfalls caused by the intermittency of wind or solar.

The hybrid model—on-site generation with a grid connection—balances reliability and flexibility. It also allows surplus on-site power to be exported to the grid when not needed by the data centre. While reliance on the grid still leaves operators vulnerable to grid connection delays, repurposing former fossil fuel sites—such as de-commissioned coal- or gas-fired power stations—could be a solution as this leverages pre-existing grid connections.

Energy parks are an example of hybrid or behind-the-metre energy supply models. These are industrial-scale energy sites where power generation (renewables, nuclear, storage) and data centre capacity are colocated, often also alongside industrial manufacturing.

The solution depends on context. Grid-tied supply remains the leading model today, but behind-the-meter and hybrid approaches are rapidly emerging as promising alternatives for meeting data centres’ growing power needs. Rather than there being a single “correct” choice, each option can be the right fit under the right conditions—its suitability shaped by the regulatory environment, commercial frameworks, and the unique energy landscape of each country.

What does the global data centre expansion mean for you and your business?

This blog post was produced by our Industry Consulting team.

We can help you understand how the data centre expansion is affecting the sector and geographies your business operates in. Our capabilities include mapping and analysing data centre build-outs, localising data centre clusters, as well as forecasting future electricity demand and implications for power generators.

If you’d like to learn more, fill in your details below or click here to get in touch.

For more detail on the methodology and data that underpins this blog post, read our report for the Nuclear Industry Association here.

Tags: