Shrinking supply delivery will support APAC CRE performance

Across Asia-Pacific, there has been a notable shift away from new development commencements

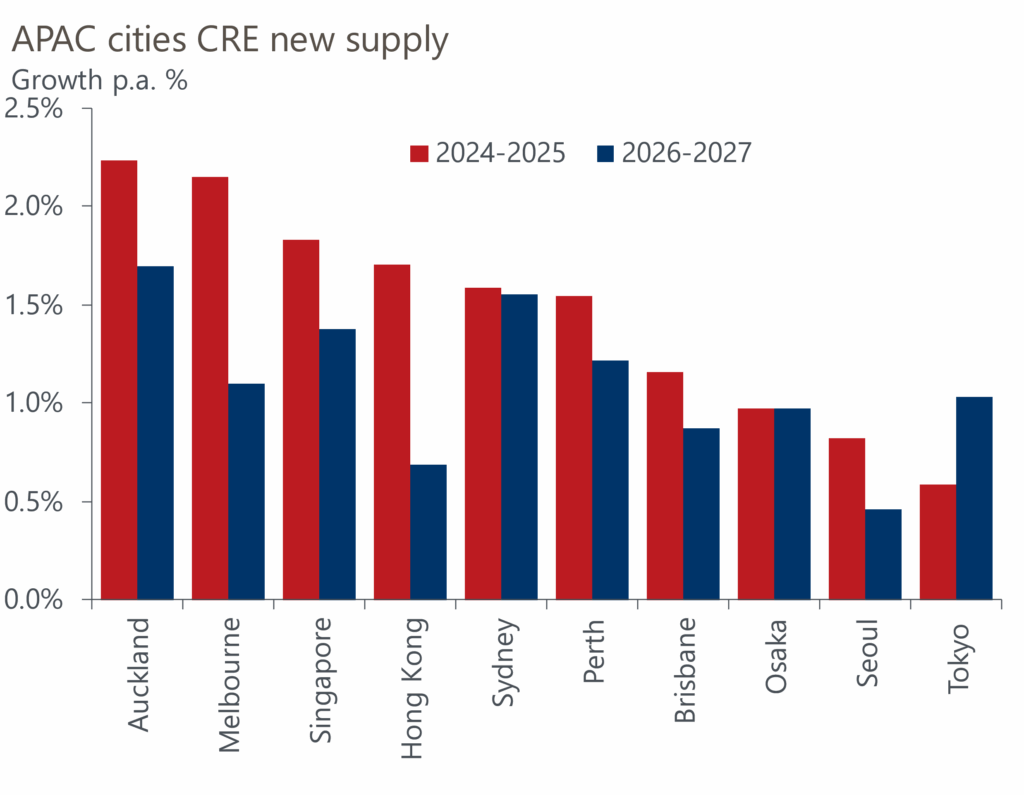

Commercial real estate development pipelines across Asia-Pacific are contracting structurally as higher construction costs, tighter financing conditions, regulatory delays, and labour shortages have undermined feasibility. The result is fewer project starts, lower land acquisitions, and a materially thinner forward supply outlook.

What you will learn in this report:

- Falling supply over the next two-three years is creating a window for operating fundamentals to improve. Vacancy rates are expected to decline and rental growth will re-emerge in offices, hotels, and select residential markets, particularly where vacancy is currently elevated.

- Supply is mainly being delivered where fundamentals are strongest. Meanwhile, development is retreating in markets with weaker demand or demographic headwinds, reinforcing divergence in performance across cities and sectors.

- The cycle has shifted toward an income-led environment in which existing assets benefit from supply discipline, industrial markets become balanced after rapid expansion, and long-term outcomes are driven by demographics, labour market trends, and capital costs rather than short-term stimulus.

Our newly expanded Real Estate Economics Service now covers 100 cities, 11 of which are in Asia-Pacific, across five major property sectors: office, retail, industrial, residential, and hotels. It includes a novel approach to estimating past and future building stock, utilising cutting-edge geospatial analytics, machine learning/AI, and big data.