Takaichi’s big win doesn’t affect the fiscal outlook for Japan

The ruling Liberal Democratic Party’s (LDP) landslide election victory on Sunday doesn’t change our expectation of a primary fiscal deficit of 2%-3% of GDP in FY2026-FY2028 – we still see the deficit only starting to decline from FY2029. We also keep our view that the 10-year Japanese government bond (JGB) yield will be at 2.3% at end-2026 and 2.5% at end-2027 and beyond.

We believe pressure from the bond and FX markets will restrain Prime Minister Sanae Takaichi’s fiscal plans. Although the election has strengthened her power base within the LDP, she still needs the cooperation of influential party members, who tend to prioritise fiscal discipline.

Her plan to cut the 8% consumption tax on food to zero for two years will likely take at least two years to implement, despite her wish to make it happen “as soon as possible”. Takaichi has also committed to identify alternative revenue sources to cover a projected decline in tax revenue.

The victory gives Takaichi more opportunity and time to tackle major policy agenda including a fundamental review of Japan’s tax and welfare framework. She described the food tax cut as a “temporary bridge” until she can introduce a refundable tax credit system designed to reduce the burden on low-income earners.

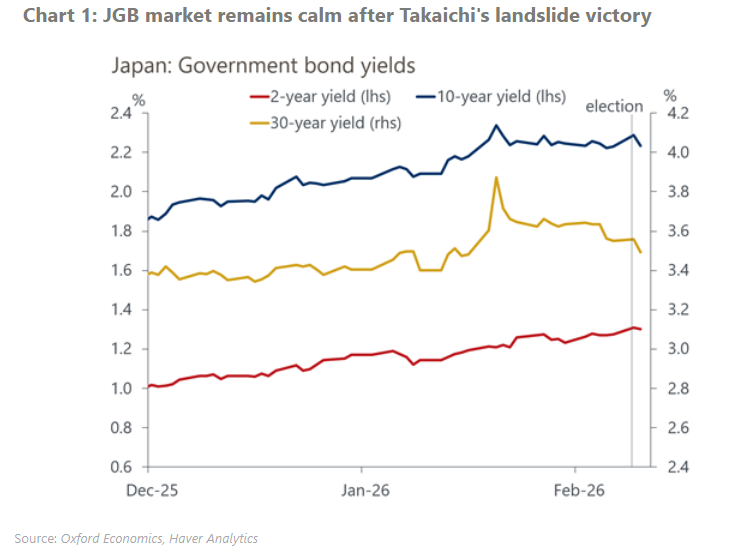

JGB yields remain calm after the election, possibly reflecting a market view that the LDP’s supermajority lowers the risk of populism-driven fiscal deterioration. But there’s still a significant risk that global investors won’t see the government’s plan to pursue both proactive fiscal policy and fiscal discipline as credible.