Research Briefing

| Dec 7, 2023

Can the banking system really rescue the property sector in China?

We are unconvinced that recent measures mark a turning point in China’s housing downturn, just as we were cautious of the efficacy of the “16-point” property support package a year ago.

What you will learn:

- The banking system can ‘rescue’ the property sector to the extent that it can reduce event or headline risk in China’s housing market, and therefore buttress activity in adjacent economic segments such as private investments and consumer spending, but it cannot ‘rescue’ the sector out of the necessary multiyear structural correction process that is underway.

- As housing struggles to find a floor, policy efforts are directed towards reinstalling confidence in private developers by alleviating ‘flow’ funding problems.

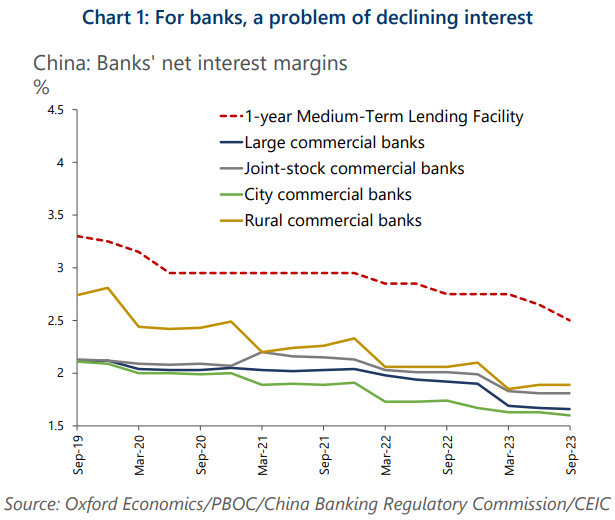

- With profitability taking a hit, large state-owned banks face the risk of further asset-quality deterioration. On the other hand, weak banks may get weaker, posing contagion risks.

- The resulting banking system is likely to be less profitable and less well-capitalised, impairing the transmission mechanism of future monetary policy. However, while the real economic impact of China’s property downturn will be sizeable and prolonged, we think ultimately, the authorities should be able to manage the downturn without it triggering a financial crisis.