Research Briefing

| Jun 14, 2024

Mild mid-year downturn before a tepid recovery emerges for Canada

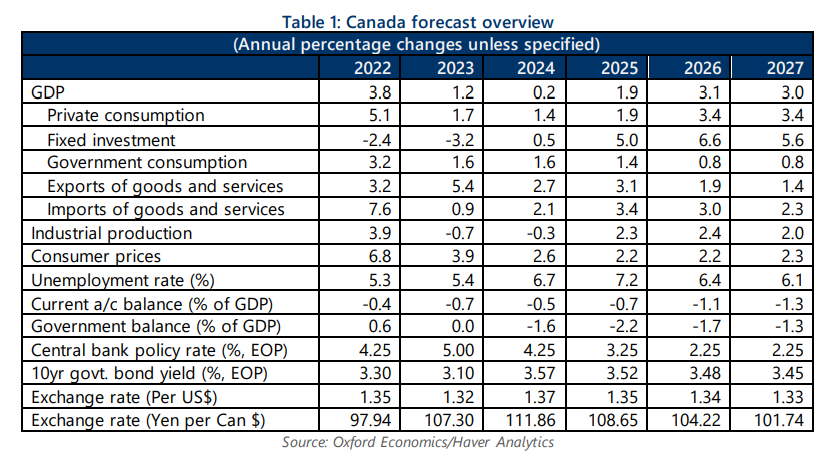

In Q1 2024, GDP grew 0.4% q/q and while the below-potential growth pace was stronger than the 0.1% rise we expected, it was weaker than the consensus view and StatCan’s preliminary estimate. We still anticipate a shallow economic downturn in Q2 and Q3 before a tepid recovery emerges later this year. Accordingly, we nudged up our GDP growth forecast by 0.1ppt to 0.2% in 2024 and lowered our forecast by 0.1ppt to 1.9% in 2025.

What you will learn:

- The rise in Q1 GDP was broad-based, with strong consumer spending on services at the heart of the pickup. But we forecast a 0.5% drop in GDP from Q1 to Q3 as the lagged impact of past rate hikes hurt consumption, new-home building, and business capital outlays.

- Slowing inventory accumulation will also be a large drag, while net exports should provide a modest buffer amid the start of oil exports along the Trans Mountain Pipeline, strong US demand, and a weaker loonie.

- Headline CPI inflation dipped to 2.7% y/y in April from 2.9% y/y in March, a hair less than our forecast. Weaker April inflation, along with a downward revision to our global oil price forecast led us to reduce our 2024 inflation forecast by 0.1ppt to 2.6%. We still expect inflation will average 2.2% in 2025 and foresee a return to the 2% target by mid-2025.