Research Briefing

| Mar 28, 2024

Japan’s Construction Outlook, March 2024

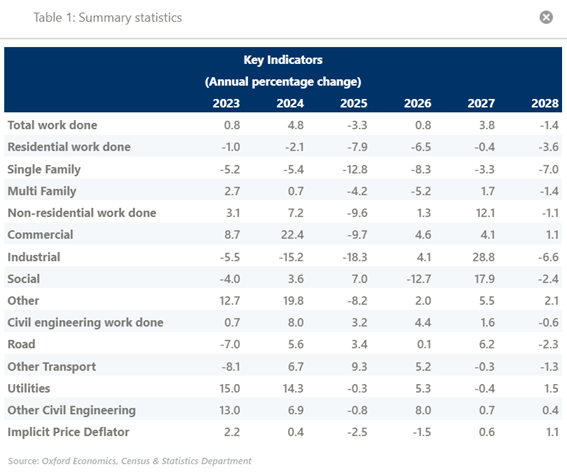

We forecast total construction work done to accelerate 4.8% in 2024. Civil engineering construction and non-residential building will drive the near term while residential building will continue to weigh on growth. Robust future capex plans will support construction activity. However, business investment has remained on a downtrend with the realisation of capex plans slow. There remains a downside risk to our forecast should expenditure plans remain slow. Nonetheless, inflation pressures are set to ease throughout 2024 and provide a boost to activity

What you will learn:

- We expect residential building is now in a persistent downtrend. Activity is forecast to fall another 2.1% over 2024. Demand for housing will be pulled down by Japan’s declining population. Consequently, residential construction activity will remain weak over the forecast horizon. Nonetheless, continued urbanisation will drive multi-family building activity in the large cities.

- We anticipate non-residential to push on from the modestly positive year in 2023 and accelerate to 7.2% growth in 2024. The sector will find key support from retail and hotel building, supported by rapidly increasing inbound tourism, now almost recovering to pre-pandemic levels. While industrial building activity will find support from the government’s supplementary budget, still depressed external demand will pull down on the sector.

- We forecast civil engineering work done narrowly returned to growth in 2023 (+0.7%) and will push on to an 8% expansion over 2024. The need to rebuild critical infrastructure after the 7.5 magnitude earthquake in early January will support activity in the near term, while a plethora of power projects continue to progress towards the target of improving Japan’s energy security and resilience.