2026 Global economic outlook conference: Top questions on AI, trade, politics and growth

In this blog, we address the key questions raised during our Global Economic Outlook Conference in London, where policymakers, business leaders and investors explored the outlook for global economic growth, AI adoption, geopolitics, trade policy and macroeconomic risks.

US: Politics, trade policy and the China Relationship

Question: How important will the US midterm elections be in terms of emboldening, or softening, President Donald Trump’s agenda and the country’s relationship with China?

Ryan Sweet, Managing Director, Macro Forecasting and Analysis

Divided government is the most likely outcome of the 2026 midterm elections. This will increase political brinkmanship around the next deadline to raise the debt limit and constrain the president’s ability to pass additional tax and spending changes, barring an unexpected crisis.

The outcome of this year’s midterms matters most for the policy battles to come under the next Congress that will preside from January 2027 through January 2029. Shifts from unified to divided governments tend to yield greater congressional investigatory activity, which will dial up the level of partisan rancor and make the bipartisanship that’s necessary to address must-pass legislation even tougher to achieve.

Changes to trade policy are more likely to stem from a potential Supreme Court ruling against most of the administration’s tariff policies and the looming renegotiation of the US-Mexico-Canada Agreement. Plus, the unfolding immigration crackdown will depend on how effectively the One Big Beautiful Bill Act’s funding boost for immigration enforcement is put to work. If the Supreme Court rules against the IEEPA tariffs and/or Trump’s economic agenda stalls under a divided government, odds are Trump will use executive orders, including tariffs. This could impact the US relationship with major trading partners, including China. We’ll get a clearer idea of how the US-China relationship could evolve in 2027 when Trump is set to meet with China later this year.

Unlock exclusive economic and business insights—sign up for our newsletter today

UK: Economic policy, growth and productivity

Question: What things could be done to improve the UK’s economic situation?

Andrew Goodwin, Chief UK Economist

In the near term, a more credible approach to fiscal policy would bolster financial market confidence and improve the chances that the consolidation is successful. Such a plan would involve reducing the reliance on tax rises and showing greater spending restraint, with a push to improve public-sector productivity being crucial to lowering spending.

The government came to power promising a focus on improving economic growth. But we’ve been underwhelmed by the policies announced so far, and would advocate a renewed focus on this issue. We’ve previously laid out our plan for growth and highlight two of our recommendations as having the potential to improve the situation.

First, we think there should be more support for investment in intangible assets, such as software, databases, and research. Investment in intangibles is a key driver of productivity growth but the UK lags well behind the global leaders, the US and Japan. Financing issues are a key constraint, and an obvious solution would be to extend the UK’s generous capital allowances for plant and machinery to include intangibles, reducing the upfront cost of investment. So far, the UK has been left behind in the race to benefit from advances in AI, but encouraging stronger investment could help make up for lost time.

Second, reforms to boost labour participation are needed. Options include:

- Additional support for childcare costs, which are quite high by European standards.

- More emphasis on getting people, where possible, off incapacity benefits and into work.

- More support for older workers.

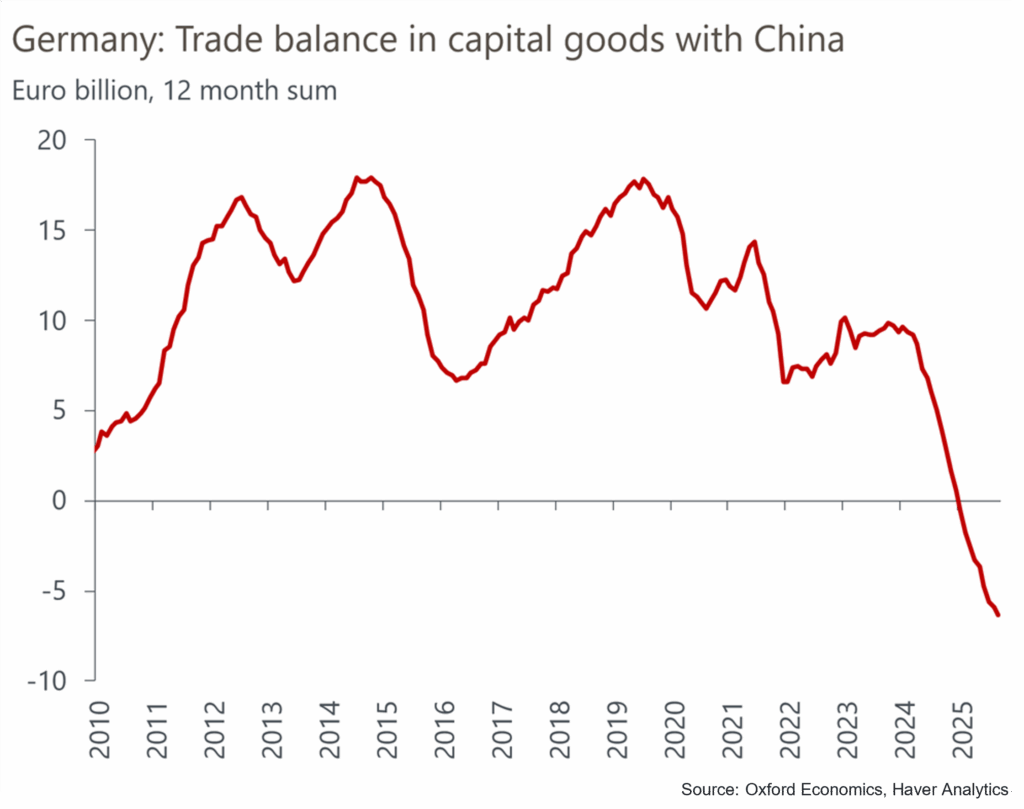

Europe: China shock and global trade imbalances

Question: What’s the risk to net exporter countries like the EU that China’s surplus continues over the next five years? If the EU puts protectionist measures in place, would that result in higher inflation?

Angel Talavera, Head of Europe Economics

We think the structural trend of large imbalances with China won’t change meaningfully over the coming years, so we expect the EU will continue to deploy corrective trade measures against China as it faces growing imbalances threatening a larger part of its industry, including key strategic sectors.

But in contrast with US policy, these measures are likely to be product- or industry-specific, be introduced gradually, and extend beyond tariffs. The EU could restrict Chinese suppliers or promote inward foreign direct investment and knowledge sharing. Although the EU would aim to comply with WTO rules, the chances of China changing its domestic policies as a result are minimal. Moreover, a stronger protective wall around the EU could divert more Chinese exports into third markets, squeezing EU exporters.

We don’t expect a major rise in bilateral tariffs between the two areas, so as a result, we don’t expect a large macro impact on growth or inflation at the moment. With limited evidence that China is dumping goods at a large scale in Europe, we don’t think targeted protective measures would represent a large boost to inflation in Europe. However, this forecast is predicated on no major escalation taking place, which will continue to be a clear risk.

China: AI, automation and growth outlook

Question: How will AI and automation shape China’s medium-term growth trajectory, and is China structurally positioned to compete for global leadership in AI?

Louise Loo, Head of Asia Economics

Artificial intelligence and automation will not transform China’s growth model the way that urbanisation or property once did – so neither a demand-led upswing or a new credit cycle – in fact, quite the opposite – but what it does is provide a structural floor to potential growth; we estimate AI and associated backward and forward linkages to add an up-to 1.0-1.5ppt contribution to annual GDP growth, offering some offset to the demographic decline.

AI impacts economies in different ways. For China, the dominant transmission channel is not consumer-facing generative AI but industrial AI, like robotics and process automation. China deploys robotics and ‘physical AI’ far more intensively than advanced economies, with pace of installation of new industrial robots the fastest in the world, according to IFR data between 2019-2023. At present, China’s comparative advantage lies less in frontier innovation and more in adoption and deployment-at-scale.

This differentiation matters. Leadership in diffusion supports productivity, export resilience, and cost competitiveness, but doesn’t generate the same rents or demand spillovers associated with upstream platform dominance. As a result, there’s a risk that the pace and use of AI in China strengthens the supply side far more than it boosts household incomes or consumption.

This also necessarily reframes the US–China AI competition as a split equilibrium rather than a zero-sum race. Clearly, the US retains an advantage in frontier model development, advanced semiconductors, cloud infrastructure, and platform ecosystems. China’s strength on the other hand, lies downstream, in applying AI at scale across production networks, leveraging on its manufacturing depth, dense supplier ecosystems, energy availability, and coordinated infrastructure investment that would materially lower the cost of deployment.

Continue the conversation: AI and the global economy in 2026

If you were not able to attend our London conference, you can join our webinar AI and the economy: your questions answered. In this interactive webinar, our economics experts from around the world will cover our latest insights on the impact of AI on economic growth, labour markets and productivity, as well as our proprietary upside and downside AI scenarios.

Register for the webinarTags: