Research Briefing

| Feb 16, 2024

Acceleration in digitalisation will keep a service trade deficit in Japan

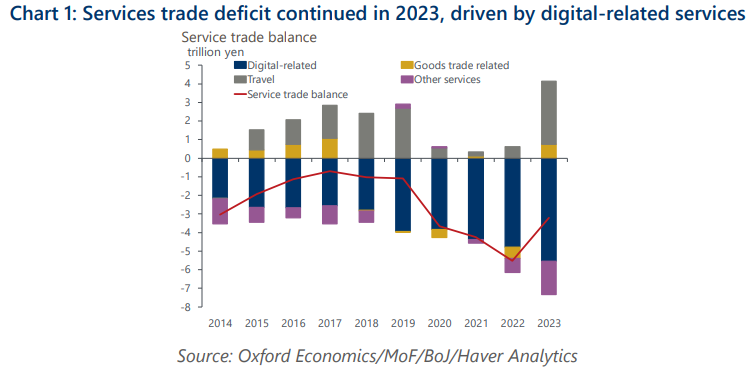

Japan’s services trade deficit continued in 2023, despite the sharp recovery to a travel surplus due to a rising number of inbound tourists after the pandemic. We project Japan’s services trade balance will remain in deficit over the coming years as a trend increase in the import of digital-related services will outweigh a rising travel services surplus that has been driven by inbound tourists.

What you will learn:

- In contrast to its success in manufacturing, Japan has been slow in moving up value chain in digital services. An aging population and the pandemic experience will accelerate the belated move toward digitalization, resulting in a demand drain through imports, especially from the US.

- The travel surplus will likely keep rising, driven by inbound tourists. However, it won’t be enough to offset the digital-related services deficit. The increase in the travel surplus will be constrained by a labour shortage in inbound tourism-related businesses and slow progress in raising consumption per head by providing higher value-added tourism services.

- Services trade deserves more attention in terms of its impact on Japan’s external balance and the FX market. Compared to goods trade, services trade has been more dynamic by responding more vividly to FX developments.