Research Briefing

| Feb 8, 2024

Eurozone: Monetary loosening will boost growth – but not until 2025

After the sharp falls in eurozone inflation recently, a series of rate cuts this year by the European Central Bank is now the consensus view. However, monetary policy transmission takes time and we don’t think growth will receive much of a boost from monetary loosening until 2025, though there’s potential for some upside surprises.

What you will learn:

- Looser financial conditions often precede actual rate cuts. Indeed, market pricing has shifted significantly following a string of downside inflation surprises in H2 2023, and despite some ECB council members pushing against early pivots, this has already delivered looser financial conditions. This easing could reverse quickly, however.

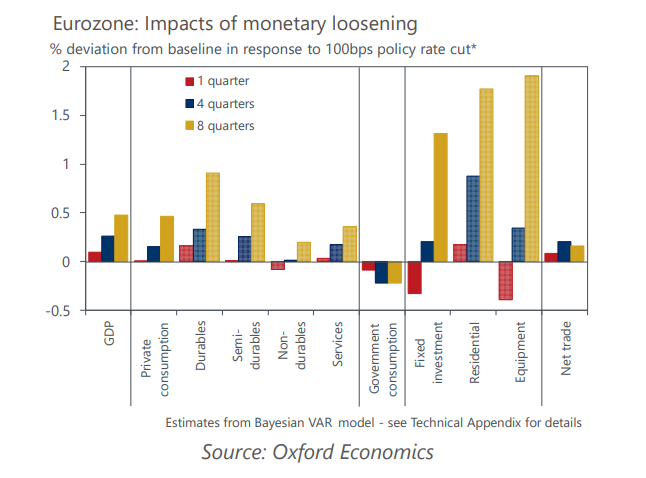

- We estimate the impact of policy rate cuts usually peaks around eight quarters later, but we see some scope for a faster pass-through in the current circumstances for both consumer and capital spending. This is due to healthier balance sheets, stronger position in the financial cycle and recent shortfalls in durables consumption and capex.

- Still, even a faster-than-usual pass-through of looser financial conditions and rate cuts won’t be a silver bullet for growth. Owing to the gradual recovery and weak base effects, we expect the eurozone GDP to only grow 0.6% this year. But we think growth will consolidate across GDP components this year, and alongside the boost from rate cuts this should generate strong growth of 1.8% in 2025.