BoJ will need to do more because of fiscal expansion

In our upcoming February forecast update, we’ll stick to our expectation of a primary fiscal deficit of 2%-3% of GDP in FY2026 and FY2027, but now think it will remain at that level in FY2028, only starting to gradually decline in FY2029 and beyond.

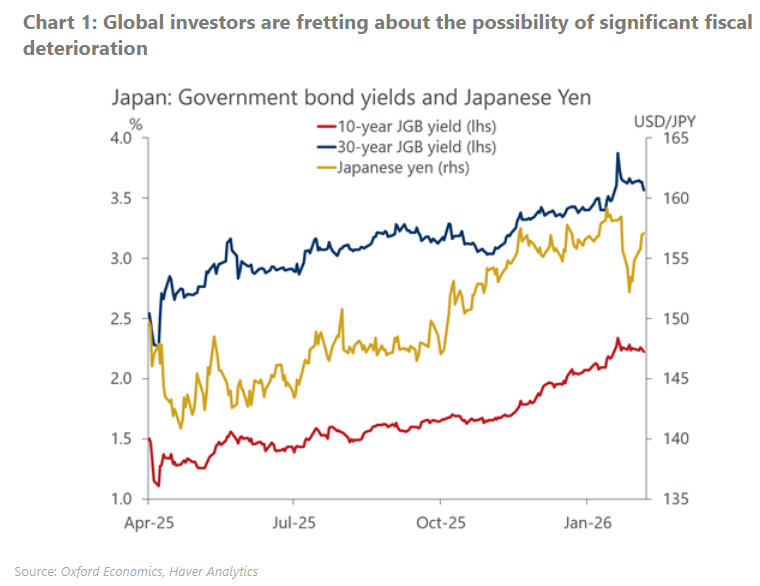

We assume that Prime Minister Sanae Takaichi will take advantage of the fiscal space generated by robust tax revenue, but maintain fiscal discipline – avoiding a rise in the debt-to-GDP ratio and further upward pressure on Japanese government bond (JGB) yields.

Based on our new fiscal outlook, we expect the debt-to-GDP ratio to remain stable until 2028, even with a higher assumption for 10-year JGB yields of 2.3% at end-2026 and 2.5% at end-2027 and beyond. We project the effective interest rate on the stock of government debt will rise only slowly, from 0.9% in 2025 to 1.6% in 2028.

We’ll also add two more rate hikes to our monetary policy forecast, given the more expansionary fiscal policy and the downward pressure on the yen. We will also nudge up our estimate of the neutral rate from 1% to close to 1.5%, by considering rising fiscal debt, higher productivity in light of the GDP revision and rising inflation expectations.

We see the Bank of Japan (BoJ) hiking every six months – June and December 2026, and June 2027. Despite more expansionary fiscal policy, we’ll raise our GDP growth forecast only marginally and see little risk of the BoJ falling behind the curve in containing demand-pull inflation.

We now see the yen staying weak at 150/USD-160/USD until 2027, driven by fiscal concerns. If the yen weakens further, it will raise the risk of more persistent cost-push inflation and mild stagflation, and the BoJ could hike faster to assure markets that it isn’t falling behind the curve..