Construction’s Next Big Shift

Rising costs, fiscal pressures, and the changing economics of construction.

Market capacity to deliver is only part of the story. An equally important question is how the next wave of construction and infrastructure investment will be paid for.

– Thomas Westrup

Australian infrastructure has ridden a public investment boom…

Australian construction work done – a measure of the cost of labour and materials fixed in place – has now risen to the same record heights in activity previously set in the second phase of the resources boom over a decade ago.

Excluding oil and gas (where construction data is distorted from importing large offshore fabricated LNG modules), Australia is building far more than back in the resource-boom days (or ever before). Correspondingly, employment in the construction sector is at a record high: over 1.3 million persons and at least 20% higher than the previous peak in activity a decade prior.

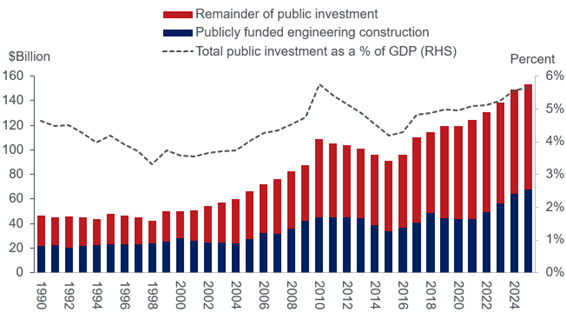

Despite publicly funded construction comprising less than one-third of sectoral activity, it has been the predominant driver of new growth in work done over the past 5 years and public investment as a share of GDP has now scaled up to reach a record high.

Figure 1. Publicly funded construction and investment, 1990-2025

The uplift in publicly funded work reflects opportunities during the post-resources boom period to use latent market capacity and low borrowing costs to invest in public infrastructure (as recommended by the IMF at the time). State and Federal Governments took that opportunity to plan and finance multi-decade infrastructure programs and megaprojects (projects valued over $1 billion) that continue to be rolled out today, with the Covid-19 pandemic providing conditions for further fiscal stimulus.

…but the conditions supporting growth in public investment have changed

The construction market today is very different to that a decade ago. In 2015, there was genuine fear in the construction industry as the resources investment boom turned to bust. Not only were future big resources projects postponed and cancelled, but the “rivers of gold” that had flowed into government coffers from the booming resources economy and royalties dried up, threatening publicly funded programs. Latent market capacity surged and construction firms were willing to accept much tighter contractual conditions and lower margins in exchange for guaranteed project work. At the same time, borrowing was much cheaper, while states such as New South Wales and Victoria had additional firepower having embarked on large asset sale programs to raise capital for infrastructure projects.

The public sector found itself in an enviable position in 2015 – access to cheap credit and the ability to strike tougher deals with construction contractors to provide value for money delivery.

Fast forward to today’s construction market and these conditions have changed substantially. Market capacity has tightened, pushing up costs on delivering infrastructure projects. Borrowing costs have also lifted sharply. Government debt is now much higher than a decade ago and the interest on this debt is rising.

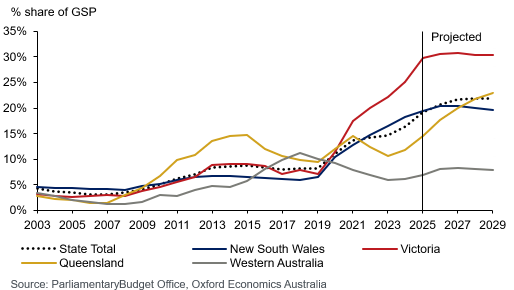

Figure 2. Gross Government Debt % Gross State Product, by state

Unsurprisingly, growth in publicly funded construction is now easing and expected to slow further over the decade. This is not uniform across all jurisdictions – Queensland being a notable exception – but at a national level, the winding down of recent infrastructure megaprojects and major programs is no longer being offset by equivalent new announcements.

Overall market capacity and cost challenges are expected to persist however, with construction activity expected to continue rising and reach successive new peaks over the remainder of this decade. This reflects a rotation in the sources of growth rather than a slowdown in underlying demand. Residential building is entering a cyclical recovery, setting up housing to lead the next cycle of investment. Alongside this, Australia faces significant long-term infrastructure needs across a widening range of sectors including energy, water, defence and data technologies.

So who pays now?

With construction activity rising above previous peaks, legitimate questions remain about industry’s capacity to deliver. But capacity is only part of the story. An equally important question is how this next wave of construction and infrastructure investment will be paid for.

While Australia’s public debt position remains comparatively manageable by advanced-economy standards – there are practical limits. Rising interest servicing costs, pressure on credit ratings, inflation and political sensitivity around deficits all constrain the scope for public infrastructure funding to continue scaling without a trade-off in other areas.

Fiscal strain, combined with the changing nature of the assets being built, will see the private sector lead the next phase of economy-wide investment and construction work done. Against this backdrop, the ability to meet Australia’s expanding infrastructure and housing needs will increasingly hinge on how effectively private financing of investment can be mobilised.

This shift is already evident in public-sector messaging, with greater emphasis on “crowding in” private capital and enabling private-led investment, such as the NSW Investment Delivery Authority’s efforts to fast-track major investment projects, Victoria’s 30-year infrastructure strategy and the Queensland state government signalling greater private sector involvement in Olympic-related infrastructure in response to budget pressures.

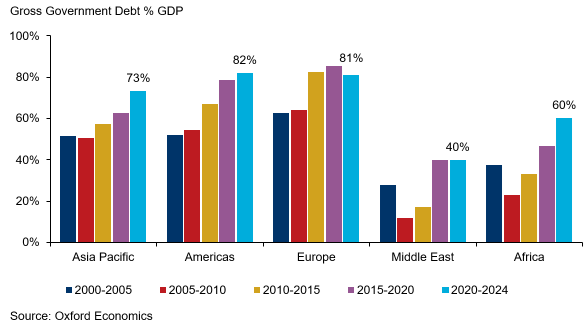

Where does Australia sit in the global perspective?

The good news is that the appetite of the private sector to invest in infrastructure is growing. Globally, institutional investors – representing pension funds and insurers – have been steadily increasing their exposure to infrastructure, drawn by the stable and long-duration returns that align with their earnings structures. This trend is particularly relevant for Australia. Supported by compulsory superannuation, Australia’s pension asset pool is on track to become the second largest in the world by 2030.

The challenge is that Australia is competing for private capital on a global scale. Many of the key investment drivers shaping Australia’s outlook – ageing assets and maintenance backlogs, rising defence commitments and the urgency of climate transition – are mirrored across advanced economies globally. At the same time, these economies are contending with progressively tighter fiscal conditions, exacerbated by Covid-era spending. As in our own backyard, this combination is pushing overseas governments towards incentivising greater private participation.

Figure 3. Gross Government Debt % Gross State Product, by state

Tapping into private finance will be critical to meet future infrastructure needs

Meeting Australia’s infrastructure and housing needs over this decade and beyond requires increasingly complex and multi-faceted solutions. Part of this will come from doing more with less – through more efficient design, delivery and use of assets (e.g. modularisation or prefabrication). The other side of the equation is expanding the pool of investable opportunities, attracting more private capital and ensuring the industry has the workforce, capability and supply chains required to deliver at scale. All of this must occur alongside the transition to more sustainable construction, with the sector directly responsible for almost one third of Australia’s total carbon emissions.

This creates interesting challenges for government and the private sector. Governments are navigating an increasingly constrained environment. Large and unavoidable infrastructure needs must be balanced against tighter fiscal conditions and the legacy of past experiences – domestically and globally – with poorly structured risk-sharing, cost overruns and delays, contingent liabilities and political sensitivities. While Australia remains a low-risk investment destination, many emerging infrastructure asset classes are inherently higher risk, requiring more innovative funding and financing approaches.

At the same time, Australia competes for capital in a global market. Project pipeline visibility, scale, packaging and sequencing all influence appetite, as does the ability to engage meaningfully with private investors and delivery partners early in the development process. Understanding how investors and contractors view the climate is critical, particularly given the irony that highly competitive, late-stage procurement has led, in some instances, to stalled delivery and poor value for money.

This is where we focus our work. At Oxford Economics Australia, we help government and industry make sense of complex investment environments – bringing together data, forecasting and construction market insight to test pipeline assumptions, understand capacity and cost pressures, and explore financing approaches that are realistic and investable.

Contact us

Complete this form and we will contact you to set up your free trial. Please note that trials are only available for qualified users.

We are committed to protecting your right to privacy and ensuring the privacy and security of your personal information. We will not share your personal information with other individuals or organisations without your permission.