Research Briefing

| Apr 11, 2024

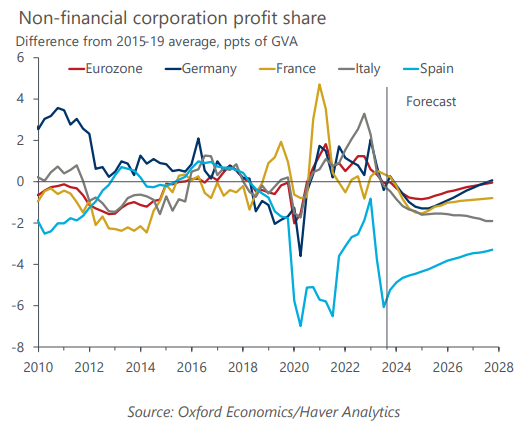

Eurozone: Corporate profit margins have further to fall

Profit margins in the eurozone have largely dropped back towards their long-term pre-pandemic average, after they increased faster than wages during the post-pandemic rebound. But we think margins will narrow further as wages catch up to inflation and productivity remains weak.

What you will learn:

- Tight supply had created shortages and an opportunity to raise margins, but the constraints have now shifted to demand, especially in the manufacturing sector where profits are still elevated. This sector has benefitted from sectoral supply-demand imbalances, though traditional profit margin indicators tend to overstate the extent of profit taking behaviour when input prices rise sharply.

- Meanwhile, profits in services are below their long-term average due to stronger wage increases.

- These trends are similar across the main eurozone economies. Spain stands out as the only major economy where profit margins are markedly below their long-term level, while the French services sector is also experiencing record low profitability.

- In the near term, we expect further compression of profit margins, offsetting the impact of high wage growth on inflation. A further drop in profits is consistent with the current weakness of the eurozone economy, as well as with the latest surveys.

- Given the subdued demand environment, we don’t think companies will be able to raise prices enough to stabilize their profit margins. Instead, corporates may try to defend their profit margins by limiting wage increases and reducing employment. This would result in weaker consumption and a softer rebound in eurozone growth than we currently forecast.