Research Briefing

| Feb 20, 2024

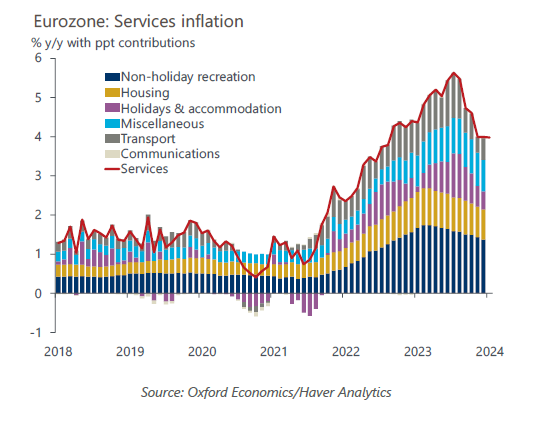

Eurozone: Stubborn services inflation should not delay rate cuts

A slower fall in services inflation will partially offset the relatively stronger disinflationary forces in goods prices. We do not think it will derail European Central Bank rate cuts this year, but the pass-through of strong wage growth from the tight labour market poses upside risks.

What you will learn:

- Services are the stickiest inflation component as labour-intensive production makes for a delayed pass-through of wage growth. However, recent strong wage growth primarily reflects a temporary catch-up for real incomes as wages react to past inflation. Several measures of wage growth show pressures beginning to abate, and as inflation falls, wages should follow with a lag.

- Firms may pass on higher wages to prices rather than reduce their profit margins, but we think there is limited scope for this given still-subdued consumer spending. Selling price expectations have fallen and are stabilising across service sectors while medium-term inflation expectations are anchored, so a more permanent upward repricing should be avoided.

- Easing price pressures elsewhere should have downward spillover effects. Oil prices have risen year to date, but the sizeable fall last year benefitted the transport sector. Falling food inflation is easing restaurant prices. Red Sea trade disruption should only have a limited, indirect impact, but much uncertainty remains on how much this may derail the broader disinflationary process.

- If there is continued progress on wage growth moderation, headline inflation eases, and growth remains lacklustre, slow services disinflation should not stop the European Central Bank from cutting rates rapidly this year. But a larger-than-assumed spillover of Red Sea trade disruption could bolster more hawkish council members to argue for slower policy normalisation.