Research Briefing

| Dec 20, 2023

India Key themes 2024 – A slowdown is coming, eventually

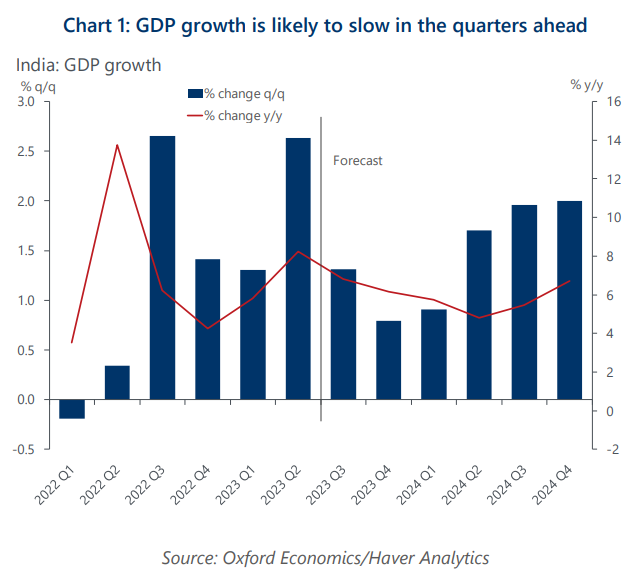

The Indian economy has been more resilient than expected in 2023, but we believe the slowdown has only been postponed rather than called off. While GDP is on track to register a strong 6.7% expansion in 2023 (6.6% in FY 2023/24), we forecast growth will slow to 5.7% in 2024 (6.2% in FY 2024/25). We think a mix of cyclical and structural themes will shape India’s economy next year.

This research report expands on these key themes:

- Private consumption and public spending will feel pandemic pains. In 2024, consumers will likely feel a dual squeeze on their spending capabilities. Labour market distress and subdued real income growth will add to the burden of higher debt servicing costs on borrowings accumulated during the pandemic. Meanwhile, although some stimulus may be provided in the run-up to the national elections, the need for fiscal consolidation will limit the government’s ability to support consumers.

- Supply-side price pressures could constrain the RBI’s room to manoeuvre, but the risks are limited. We expect the RBI to start cutting rates in Q2 2024 as we believe the conditions for it to do so will be met by then, including slowing economic activity, declining core inflation, and confidence that headline inflation is settling close to target. But pressures beyond the RBI’s control may mean that even though domestic conditions call for lower rates, actual cuts may take longer.

- More structural improvements are crucial for leveraging India’s demographic dividend. India overtook China as the world’s most populous nation earlier in 2023, and the size and youthfulness of its population bolster the economy’s enormous growth potential. Its current services-based model, however, means creating the right jobs to achieve sustainable and inclusive growth will be challenging, though not unachievable if the right structural reforms are in place.