Research Briefing

| Aug 15, 2024

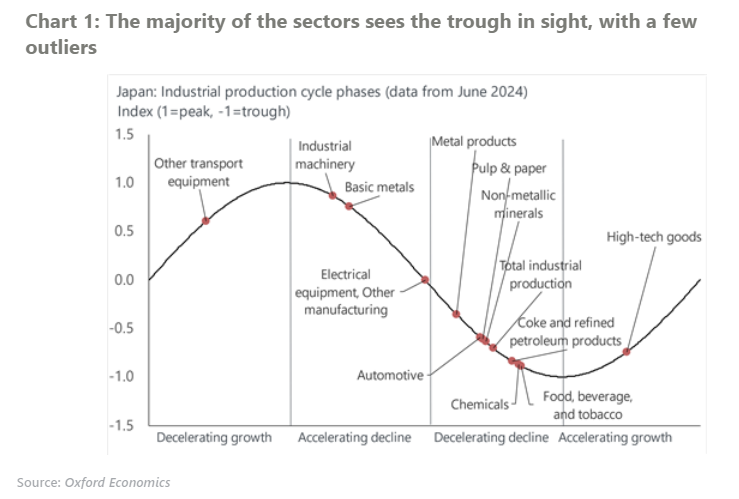

Japan’s industry nearing the trough, with high tech leading the way

Our new proprietary business cycle phase indicator points to a trough in sight for industry, but with dispersion among sectors. High tech is leading the pack with output firmly on its way up. While most other sectors have yet to reach a cyclical trough, we believe they are now closing in.

What you will learn:

- Output of high-tech goods has been growing since the beginning of 2024 largely thanks to higher semiconductor production, notably bucking the downward trend across much of industry. We see momentum only strengthening from here, and at 4.1% growth for 2024, the industry is forecast to be one of the fastest-growing manufacturing sectors this year.

- Industrial machinery is on the other side of the spectrum, as it appears the slowdown since the end of 2022 is set to intensify. The softness is apparent across the board but is more pronounced in subsectors such as metal forming machinery, where a long inventory adjustment process appears inevitable.

- The auto sector’s position in the phase indicator is heavily distorted by the recurrent production stoppages stemming from the safety testing scandal. Absent these distortions, the sector would most likely be in the decelerating growth or accelerating decline phase.

- Chemicals have been declining since early 2022 due to higher energy prices but the turning point is close. The gradual appreciation of the yen will lower energy costs and support profit margins, although tighter monetary policy and the destocking cycle will keep growth in check.