Research Briefing

| Mar 7, 2025

Japan’s older households to support spending under higher rates

The resilience of consumption is essential to support sustained wage-driven inflation and the Bank of Japan’s rate hikes. We see little risk of spending faltering due to the projected gradual rate hikes to 1% because the ageing of society has made households’ balance sheets less vulnerable to rate increases.

What you will learn:

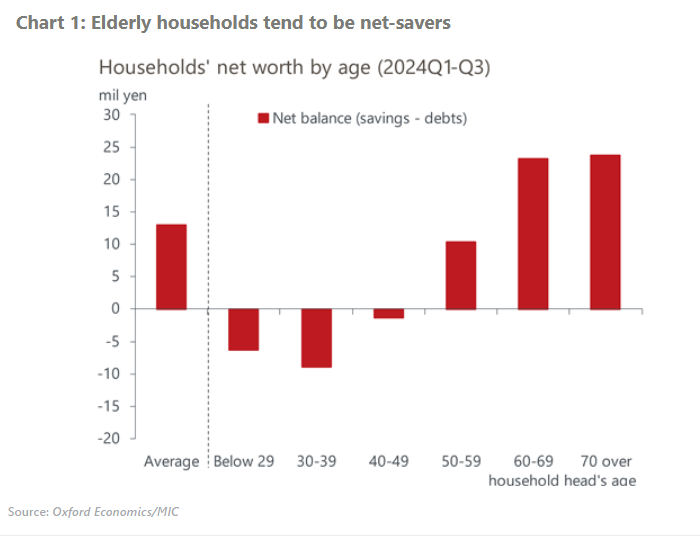

- Today, 35% of the Japanese population is older than 60, while their share of the consumption market is about half. We think their consumption will remain firm, given they tend to be net savers, implying that higher interest rates will have positive impacts on their balance sheets. For retired households, stable gains in pension benefits are also supportive.

- In contrast, households in their 30s and 40s tend to be net debtors due to large mortgage balances that are overwhelmingly floating rate loans, making them vulnerable to higher rates. At the same time, they benefit from pay rises which will likely outweigh the increased interest expenses in our baseline projection.

- We think that risks to consumption outlooks are tilted toward the downside. Supply-driven inflation could hamper households’ real income recoveries, if it proves more persistent than projected. Uncertainly about inflation and interest rates could increase precautionary savings by younger generations, which have been on a trend rise in the past years.