Research Briefing

| Sep 24, 2024

Japan’s rising labour turnover will raise productivity, but only slowly

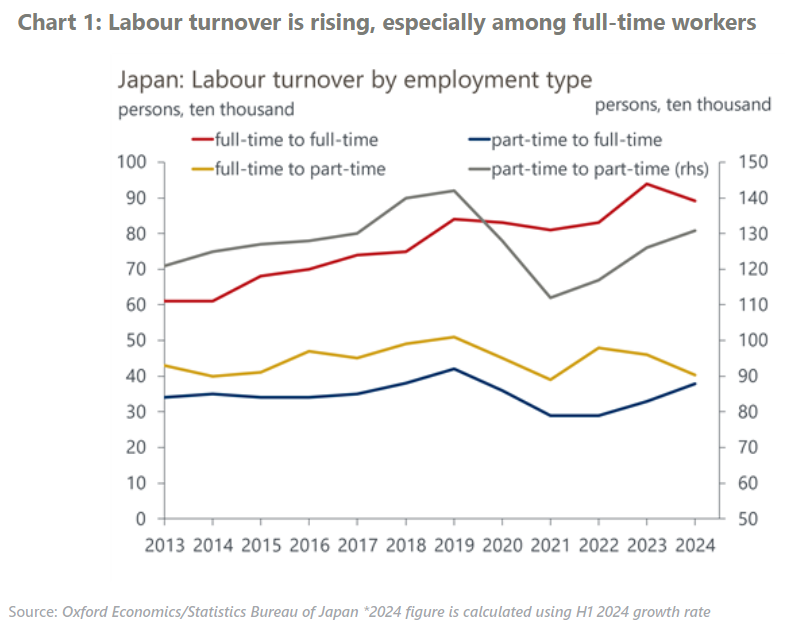

Labour turnover is quickly rising among full-time workers in Japan, where long-term employment has been prevailing. Although a serious labour shortage and a sharp rise in labour turnover will provide a great opportunity and incentive for productivity improvement, we this this will occur only gradually.

What you will learn:

- Rising labour turnover, especially among young workers, has enhanced the ongoing wage-driven inflation process by changing the employment system in Japan, which has been characterized by the combination of long-term job security and a rigid seniority-based wage scale.

- Within same industries, employment has shifted from small firms to large firms. This change in the distribution of labour will likely accelerate as unprofitable small firms fail. The shift will raise productivity in those industries where the gap in productivity between large and small firms is significant.

- But progress in the reallocation of labour through turnover across industries has been limited. Changes in the share of labour input by industry have made only a modest positive contribution to overall productivity growth and its impact has become smaller in recent years.

- Labour turnover across industries will rise, but only gradually because it requires re-skilling of workers and the reallocation of workers across regions. Despite some positive impact from AI, we maintain a cautious projection of long-term productivity growth in Japan.