Research Briefing

| Mar 18, 2025

Japan’s supply-driven food inflation to persist longer than expected

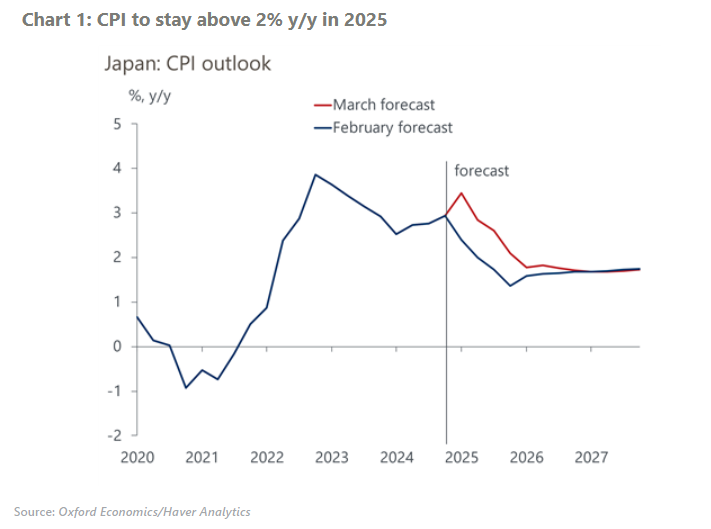

We have revised our CPI forecast upwards for this year and next, due to more persistent supply side-driven food inflation, led by soaring prices of rice. Despite the significant revision to the short-term inflation path, we don’t expect the Bank of Japan (BoJ) to react with a rate hike.

What you will learn:

- A combination of record summer heat in 2023, panic buying, and speculative trading has driven rice prices upwards. Despite a good harvest in 2024 and the government’s decision to sell its rice stockpiles, prices are still rising and we now expect them to decline more slowly than we previously anticipated.

- The prices of non-fresh foods other than rice have also registered modest but persistent inflation, of 3%-4%, reflecting the pass-through of rising input costs, including the lagged impact of yen weakening and a sharp rise in logistics costs.

- We have not changed our monetary policy forecast since the supply-driven food inflation, especially rising rice prices, will likely stabilise. That said, we will closely monitor how higher food inflation affects inflation expectations. We have nudged up our 10-year Japanese government bond (JGB) forecast to reflect a higher inflation risk premium.