Research Briefing

| Dec 19, 2023

No change in policy as BoJ waits for wage data

The Bank of Japan left both short-term and long-term policy rates unchanged at Tuesday’s meeting. Amid a decline in global yields, pressures on the Yield Curve Control (YCC) policy framework from bond and foreign exchange rate markets have eased.

What you will learn:

- Recent data confirm our view that inflation will continue to decline for several quarters pressures from past import inflation abate. More data on the 2024 spring wage settlement is needed to assess the prospect of achieving the 2% inflation target in the coming years.

- Meanwhile, the BoJ’s review of monetary policy is progressing. At a recent workshop, the bank’s staff papers argued that past easing has “contributed to creating a non-deflationary environment,” but it estimated this added only about 1ppts to the inflation rate.

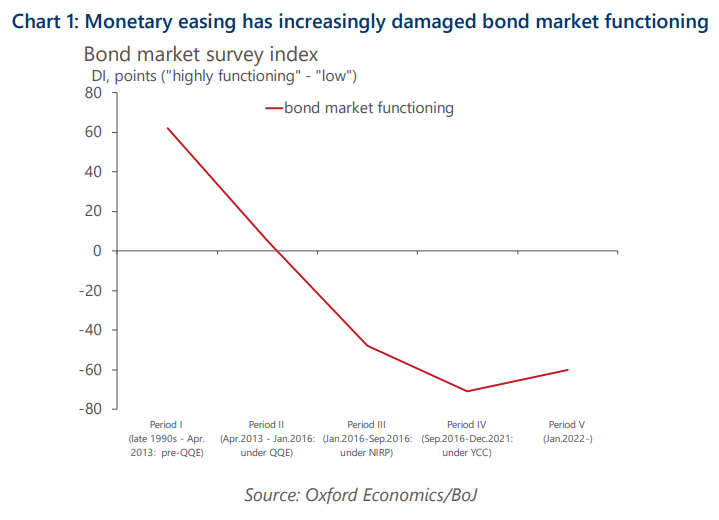

- The staff papers highlighted the negative side-effects on bond markets from aggressive quantitative easing and the introduction of unlimited fixed-rate purchase operations to defend the YCC ceiling. The papers also showed the side-effects of the negative interest rate policy.

- We maintain our call that the BoJ will abolish the NIRP at the April meeting next year after confirming a robust spring wage settlement.

- The ‘review’ is expected to be concluded in mid-2024 but the BoJ will not rush to exit QE in our view. The exit will be delicate, requiring many years and comprehensive policy measures in conjunction with the government to ensure a smooth and stable process.