Research Briefing

| Mar 15, 2024

Nordics: Growth to pick up this year, but it will diverge

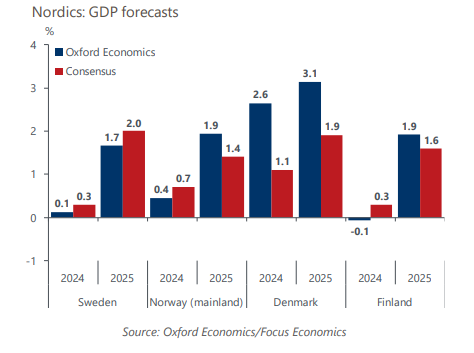

The Nordic economies will have a better 2024 than last year, but growth rates will diverge across the region. The main growth drivers will be improving domestic demand, higher confidence, and easing financial conditions amid lower inflation and policy easing. A pharma boom will make Denmark outperform, while a weak finish to 2023 will weigh on growth in Finland and Sweden.

What you will learn:

- Confidence has improved across all sectors, indicating that the worst is over. Lower inflation, still tight labour markets, and positive real income growth should translate to higher private consumption. Interest rate-sensitive fixed investment will resume growth as rates decline.

- Headline inflation will continue to decline faster than core inflation, which is more affected by strong wage growth. We expect that energy and food prices, which have been the main drivers of the initial inflation surge, will continue to be the main drivers of the disinflation. Disruptions to Red Sea shipping should not derail disinflation, but they present an upside risk.

- Attention has turned towards the timing of rate cuts as growth slows and underlying price pressures abate. We expect Sweden’s Riksbank to commence with rate cuts in May or June, but Norway’s Norges Bank will stay on hold until December. Currency developments in both countries will remain important factors in central bank policymaking this year.

- Easing financial conditions will pass through to the economy relatively quickly, due to the prevalence of variable rate loans. This will be a key driver for improving demand; its weakness has become the main factor limiting output.