Powering Growth: How Data Centres Are Reshaping APAC Economies

Asia is in the middle of a data centre gold rush. China, India, and other markets are racing to realise the benefits of Generative AI, with new models that demand massive compute and energy. Today, Asia sits second in global data centre market share, behind North America, and the growth in capacity is set to expand by double digits over the next few years. This momentum is drawing billions in capital expenditure into hyperscale campuses, grid connections, and fibre routes, rapidly building the digital backbone of APAC’s economies.

Navigating the trade-off between economic and environmental goals

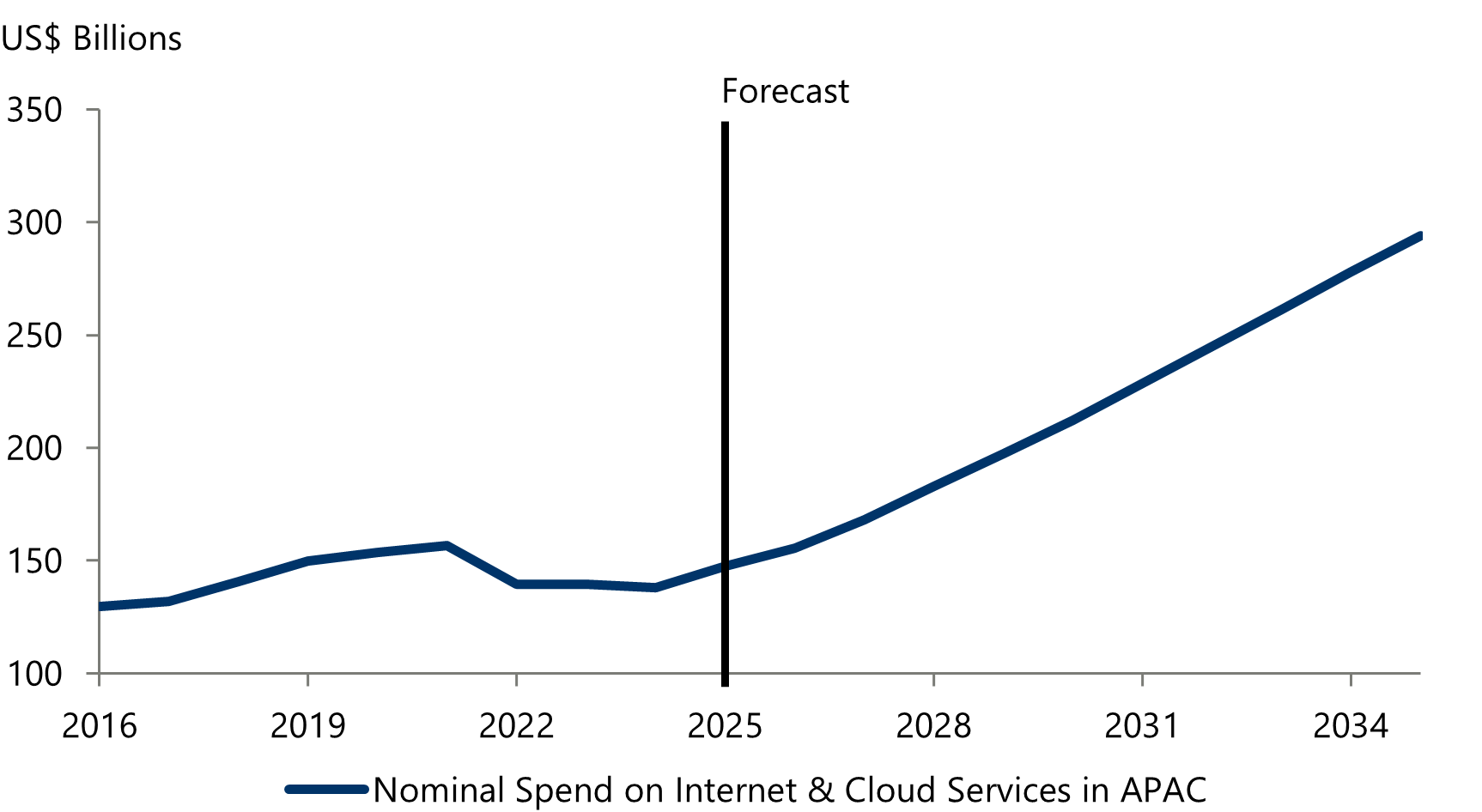

Accelerating investment is driving a rapid buildout of data centres. Oxford Economics projects that spending on internet and cloud services will nearly double to about US$300 billion by 2035 (Fig. 1).

Figure 1: Nominal Spend on Internet & Cloud Services in APAC

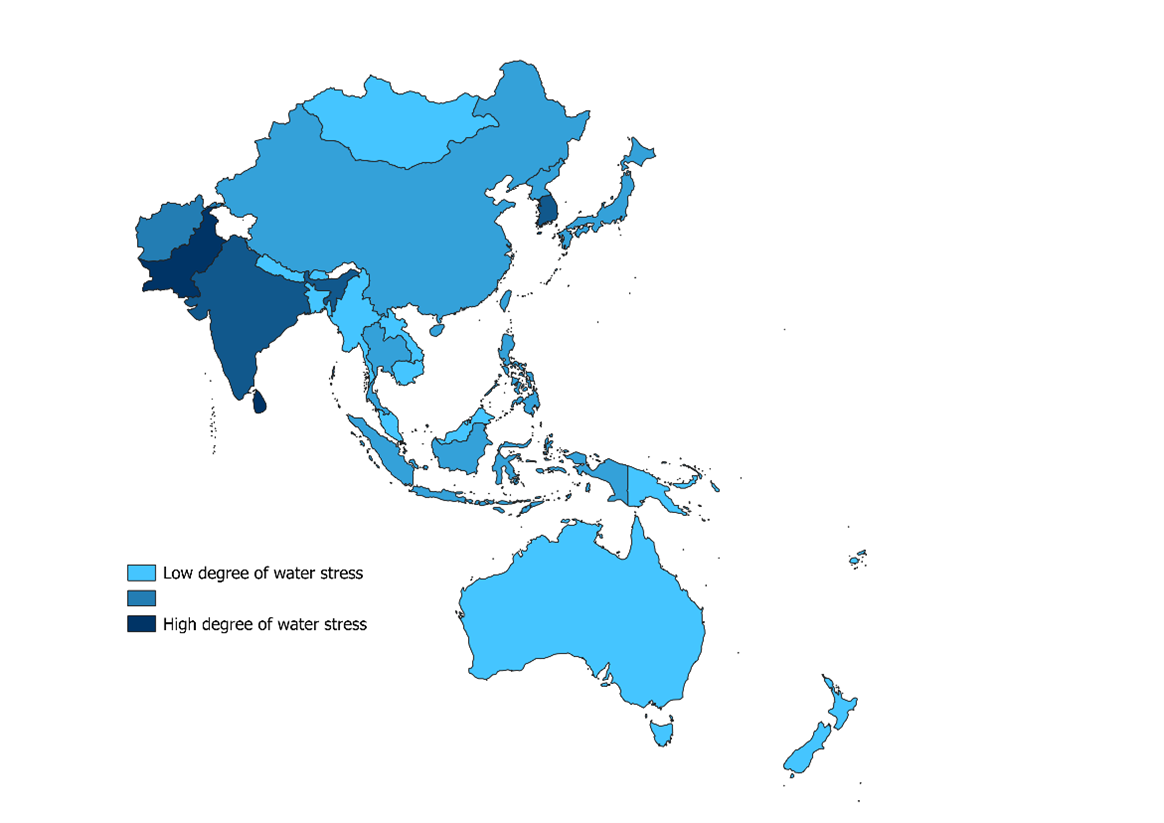

Asia Pacific is expected to nearly double its data centre capacity to 57 GW by 2030.1 Yet the region’s power mix remains dominated by fossil fuels, and some regions face acute water shortages, meaning the data centre expansion creates an energy and climate dilemma.2

Many economies in Central, South, and East Asia already face high water stress (Fig. 2), and additional demand from data‑centre cooling could intensify local pressures. Operating conditions compound the challenge: hot, humid climates raise cooling loads; land and water constraints are binding; and limited headroom to add renewables and grid capacity quickly heightens the risk.

Figure 2: Degree of water stress across APAC

In dense urban hubs, data centres can account for a significant share of electricity demand and sectoral emissions. The mandate for governments and operators is clear: keep scaling top‑tier compute while materially reducing energy intensity and water use.

Powering Growth: How Data Centres Are Reshaping APAC Economies

During the construction phase and into operations, spending by data centre operators and their tenants supports jobs and wage-incomes across a wide ecosystem of builders, suppliers, transport, and professional services. This spending circulates through households and local businesses, leading to direct, indirect, and induced economic impacts that can be measurable at city, provincial, and national levels.

This footprint can be meaningful in localised areas, but does not do justice to the data centre’s main economic value proposition – the larger economic contributions from data centre investments are catalytic in nature.

The larger economic impacts from data centres arise through two principal channels:

The first is through agglomeration effects. Data centres concentrate low latency, highly reliable connectivity that attracts data intensive users and service providers and encourages clustering around key nodes. This lifts productivity by cutting delays and failures, supports compliance in regulated sectors, and reduces the cost of digital operations, especially for MSMEs with limited IT resources. Modern interconnection points further strengthen resilience through greater route diversity and faster recovery, resulting in fewer interruptions and more predictable operations as cloud adoption becomes easier for smaller organisations.

The second is through workforce and capability effects. While onsite headcount in data centres remains lean, operators and vendors expand the pool of technicians and operations staff, often in partnership with education and training institutions, and help formalise work and safety practices across the supply chain.

From Narrative to Numbers: Turning Local Investments into National Gains

So often the headlines criticise the low employment headcount attached to data centre operations, but this misses their true contribution. Data centres have proven to anchor investment within a local economic area, whilst raising productivity and reliability across the economy, and attracting complementary capital in connectivity and power.

Demonstrating the economic proposition of a data centre project requires a broader lens – with quantitative analysis of economy-wide impacts, not just direct employment and expenditure. Because these catalytic effects diffuse through supply chains and productivity channels, they are often overlooked in job-centric narratives about data centre impacts. Rigorous economic assessment can link local investments to improvements in both economic and non-economic national outcomes, from higher GDP, improved productivity, and a broader fiscal base to stronger data sovereignty, enhanced national security, and more resilient essential services.

At Oxford Economics, we help you surface and quantify those contributions, turning anecdotes into evidence.

Our Economic Impact Consulting team builds defensible models that capture direct, indirect, and induced impacts, plus catalytic effects that are often missed, such as supplier development, skills formation, productivity gains, and infrastructure upgrades. We translate your operational data into board and regulator ready insights on jobs, GVA, incomes, and tax across construction and operations, at city, provincial, and national levels. We also run forward looking scenarios, including AI driven load growth, power and carbon forecast, and policy shifts, so you can credibly articulate both today’s impact and tomorrow’s trajectory.

The result is a clear country-level value story that strengthens stakeholder trust, informs site selection and incentives, and helps you scale with confidence.

- JLL, “2026 Global Data Center Outlook” , accessed January 2026. ↩

- International Energy Agency, “Total energy supply, Asia Pacific, 2023” , accessed January 2026. ↩