Research Briefing

| Dec 6, 2022

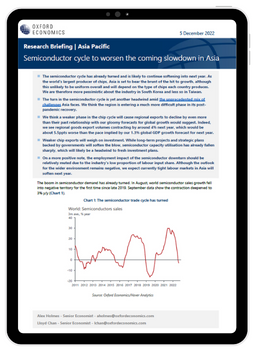

Semiconductor cycle to worsen the coming slowdown in Asia

The semiconductor cycle has already turned and is likely to continue softening into next year. As the world’s largest producer of chips, Asia is set to bear the brunt of the hit to growth, although this unlikely to be uniform overall and will depend on the type of chips each country produces. We are therefore more pessimistic about the industry in South Korea and less so in Taiwan.

What you will learn:

- The turn in the semiconductor cycle is yet another headwind amid the unprecedented mix of challenges Asia faces. We think the region is entering a much more difficult phase in its post-pandemic recovery.

- We think a weaker phase in the chip cycle will cause regional exports to decline by even more than their past relationship with our gloomy forecasts for global growth would suggest. Indeed, we see regional goods export volumes contracting by around 4% next year, which would be about 5.5ppts worse than the pace implied by our 1.3% global GDP growth forecast for next year.

- Weaker chip exports will weigh on investment. While long-term projects and strategic plans backed by governments will soften the blow, semiconductor capacity utilisation has already fallen sharply, which will likely be a headwind to fresh investment plans.