Research Briefing

| Feb 27, 2025

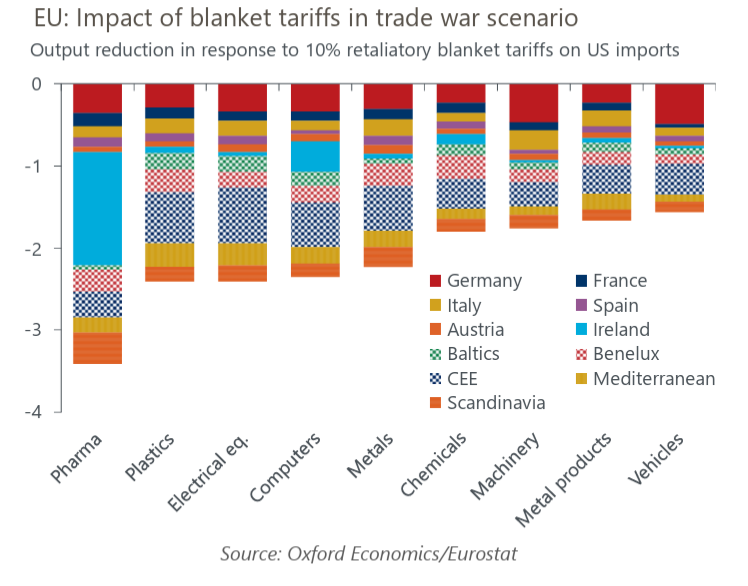

Tariff impacts expose vulnerabilities in Ireland and CEE

Blanket 10% tariffs on EU exports to the US, now part of our baseline, will have a significant but uneven sectoral impact. Our industry-level modelling suggests that the pharmaceutical and high-tech industries would be the most affected. Similarly, smaller, less diversified economies are more exposed. We estimate that Ireland and Central and Eastern European (CEE) economies will experience the largest hit.

What you will learn:

- Notably, it’s not countries with the highest direct exposure to the US suffering the most, but those indirectly impacted via integrated EU supply chains. This is particularly pronounced in the automotive sector, where Germany’s large support industry located in parts of CEE and Austria faces a more significant reduction in output than that of the German industry itself.

- Declines in industrial electricity prices through 2025 should reduce cost pressures in highly energy-intensive sectors where output remains weak, allowing for a partial output recovery.

- Opting for targeted tariffs instead of blanket tariffs could exacerbate the impact on some EU industries. We simulated a scenario with 25% tariffs only on metals, cars, and pharmaceuticals. We found similar results to our blanket tariffs scenario but with stronger effects for Ireland and Denmark due to pharma, and for Germany and Slovakia due to automotive.

- The risks around our estimates are balanced. We assume a strong pass-through of tariffs to prices and uniform price elasticity across products and countries. However, we exclude potential competitiveness boosts from a weaker euro and assume limited substitution towards alternative suppliers. At the margin, we anticipate larger effects in sectors with a higher share of exports directed towards final demand, due to stronger price elasticities.