Research Briefing

| Nov 29, 2022

The challenge for Bank Indonesia

Bank Indonesia raised its policy rate by 50 bps at its last meeting on November 17, making for a total of 175bps of rate hikes over the last 6 months. We think that rate increases are likely to end soon with two more increases of 25bps, or total of 50 bps, still to come in this cycle.

What you will learn:

- Moreover, we think the risks are skewed to rate cuts earlier than in our baseline forecast, largely due to our expectation of a stable rupiah and waning domestic inflation.

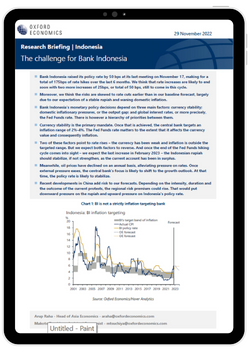

- Bank Indonesia’s monetary policy decisions depend on three main factors: currency stability; domestic inflationary pressures, or the output gap; and global interest rates, or more precisely, the Fed Funds rate. There is however a hierarchy of priorities between them.

- Currency stability is the primary mandate. Once that is achieved, the central bank targets an inflation range of 2%-4%. The Fed Funds rate matters to the extent that it affects the currency value and consequently inflation.