Research Briefing

| Jun 10, 2024

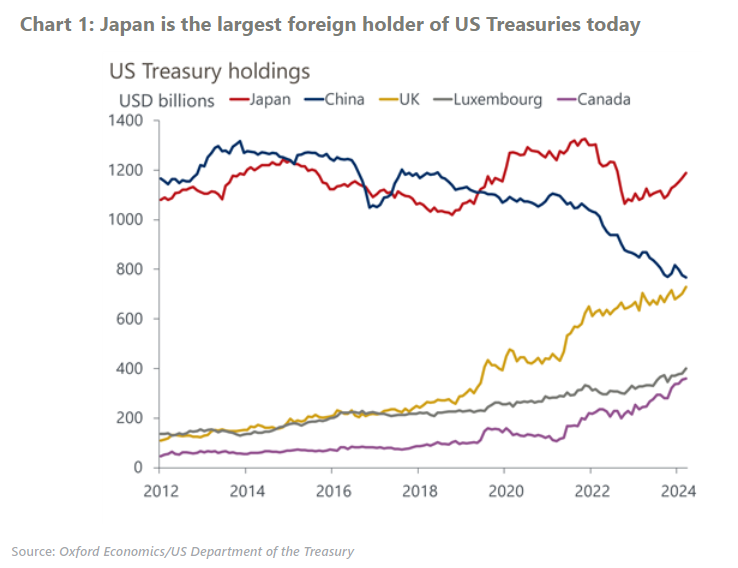

The enduring appeal of US Treasuries to Japan’s investors

Some market participants are raising concerns over a fall in demand for US Treasuries from Japanese investors amid higher domestic yields. But we think that there will continue to be a large and stable investor base in Japan for US Treasuries due to the still-large yield gap. Also, uncertainty over the Bank of Japan’s monetary policy is dissuading investors from increasing their holdings of Japanese government bonds.

What you will learn:

- After a sharp drop in Japan’s US Treasuries holdings in 2022 as US yields rose, commercial banks restored their foreign bond portfolios in 2023. Pension funds have also maintained steady purchases in foreign bonds following their mid-term asset allocation. Life insurers are the only group to have continued to reduce foreign bond holdings as hedging costs have been elevated.

- We expect Japanese investors will increase their US Treasuries holdings gradually, following a turn in bond market trends and backed by persistent yen weakness. Even life insurers will likely resume their investments in US Treasuries without FX hedges probably in Q4 2024, while steering away from hedged bonds.

- We don’t think Japanese investors will shift their portfolio allocations to domestic assets any time soon, notwithstanding the recent pick-up in domestic yields. The expected total return of JGBs is still considerably lower than US Treasuries in yen terms. For lifer insurers in particular, the current 30-year JGB yield level is only slightly above average procurement interest rates of around 2%. In addition, expectations of a continued rise in yields fuelled by uncertainty in Japan’s monetary policy over the mid-term is precluding a swift return to JGBs by domestic investors.