Research Briefing

| Apr 26, 2024

The euro and depreciation – shake, shake it off

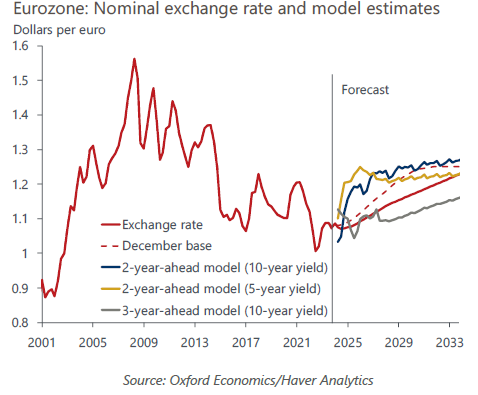

Our new forecast assumes a slower euro appreciation against the dollar over the coming years than we previously anticipated. Relative productivity, terms of trade, and the current account will likely be less supportive of the euro than we thought. In addition, a stronger stock market than initially envisaged will attract more financial flows into the US than we had expected.

What you will learn:

- We think that the euro will remain weak but, in broad terms, will not depreciate more this year. An energy prices-related negative terms of trade shock is unlikely, and news on US inflation should be less negative in the next few months.

- We expect the euro to start gaining value next year. A faster pace of Fed rate cuts than currently priced in by the markets would shrink the real yield differential in the euro’s favour. The higher relative return will make euro-denominated assets more attractive and support the currency.

- Further ahead, productivity should recover as temporary drags fade, supporting the euro. Workforce utilisation has been suboptimal due to labour hoarding by firms and the ongoing adaptation in the production structure. In addition, the strength of lower value-added services has exacerbated the weakness in productivity due to a compositional effect.