US renewables industry already reaping benefits from the Inflation Reduction Act

The Inflation Reduction Act (IRA) that came into force in the US at the beginning of 2023 is a game-changer both in terms of its size and its reach. Our research study with Energy UK (the trade association for the UK energy industry) shows it has already had a triple-whammy effect, increasing the number of new clean energy plants under construction, expanding shipments of equipment, and raising stock market valuations of low-carbon technology firms.

With a planned budget of $369 bn from 2023 to 2031, the IRA is one of the world’s largest-scale investment incentive regimes. More than half of the funds will be used for corporate tax credits that will cover a wide range of energy sources and technologies.

To determine the extent to which these schemes are likely to stimulate growth in the renewables sector we analysed the preliminary evidence on its potential impact on boosting investment in clean technology in the US. Although the act only came into force on 1 January 2023, there has already been some positive anecdotal evidence. For example, Bloomberg NEF reported in April that since the passage of the IRA, automotive and battery sectors had announced $52 billion in planned new factories—more than 20 times the amount announced in 2021.

We examined three sources of high frequency data. The first were US Census Bureau figures on manufacturers’ shipments of power transmission equipment and batteries. This showed a strong uptick, especially of batteries. This alone isn’t a clear signal, however, as other factors such as the post-pandemic recovery and the easing of supply chain bottlenecks may have been at play.

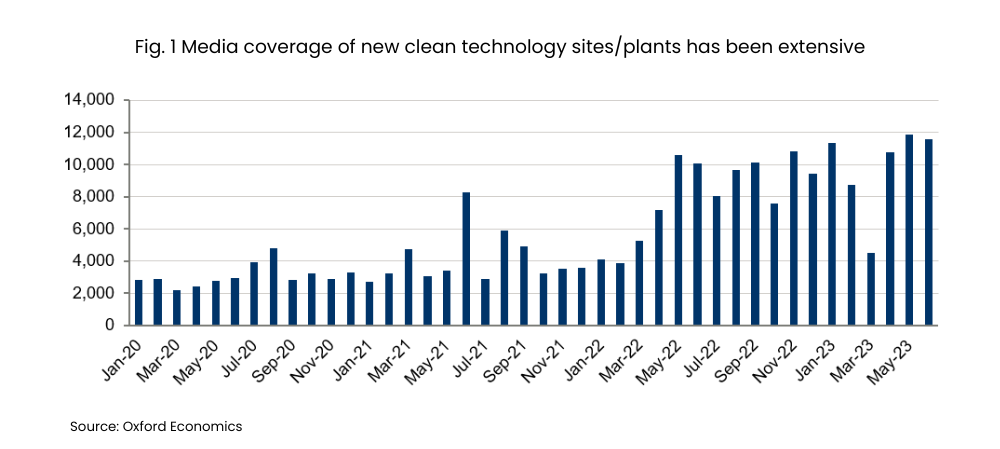

Next we carried out a search of US media mentions of new low-carbon technology sites such as solar, batteries, electric vehicles, nuclear, and offshore and onshore wind. These have nearly doubled since the act was announced, with average monthly media mentions for new clean technology sites/plants in the US more than doubling to 9,700 between August 2022 and June 2023 from 4,400 between January 2020 and July 2022 (Fig. 1).

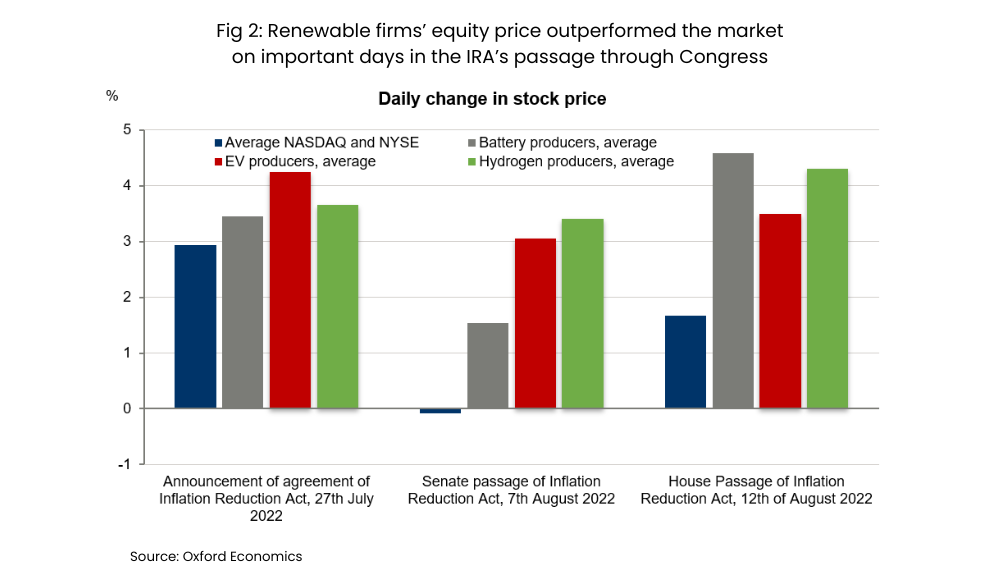

The third piece of evidence was based on share price data analysis for US-based companies specialising in low-carbon technologies, which reflect how profitable investors believe these companies will be in the future. We found that US clean technology companies listed on NASDAQ or the New York Stock Exchange reported higher daily percentage changes in their share price than the average of the host indices on three key days:

- 27 July 2022, the day of the bipartisan announcement on the content of IRA. The stock market rose 2.9%, EV producers enjoyed a 4.2% rise, hydrogen producers 3.7%, and battery producers 3.5%.

- 7 August 2022, when the US Senate passed IRA. Hydrogen firms jumped 3.4%, EV makers 3.1%, and battery producers 1.5%, compared with a 0.1% fall in the NASDAQ and NYSE.

- 12 August 2022, when the US House of Representatives passed the act. Battery producers’ shares jumped 4.6%, hydrogen producers’ 4.3%, and battery producers’ 3.5%—outstripping a 1.7% rise in the US market.

Our analysis suggests that even at this early stage investors see the act as a positive stimulus for clean technology companies’ future profits. This is likely to give the US a competitive advantage in the development and commercialisation of hydrogen and other new clean technologies, and may fuel long-term growth for companies in many associated sectors.

Authors

Contact us to find out more about our industry consulting services.

Tags: