Research Briefing

| May 6, 2021

US | The changing face of manufacturing’s rebound in 2021

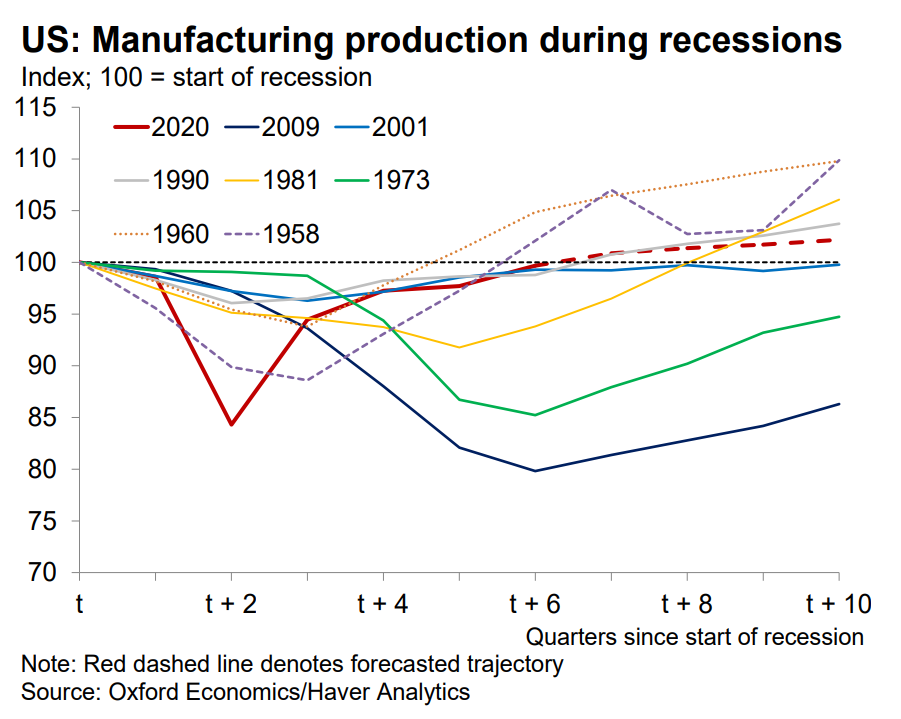

US manufacturing activity is currently above pre-coronavirus levels, marking

the fastest and strongest recovery in the past 60 years. A durable goods snapback in the latter half of 2020 powered the rebound, while nondurables

recovered more slowly. With manufacturing output now above its pre-recession level, we anticipate the recovery dynamics will flip this year, with growth in nondurables taking the lead.

What you will learn:

- Robust demand for automobiles and computers and electronics supported manufacturing’s rapid comeback in H2 2020.

- Looking ahead, nondurable goods will lead the manufacturing sector’s recovery in 2021. Chemicals, food and beverage, and petroleum and coal will be the main sources of growth.

- With more than half of states having recouped their pandemic-induced losses by the end of 2020, we expect all states to make up their losses by Q2 2021.