Why Gulf cities are strongly positioned to scale in the AI value chain

By Mohamed Majed

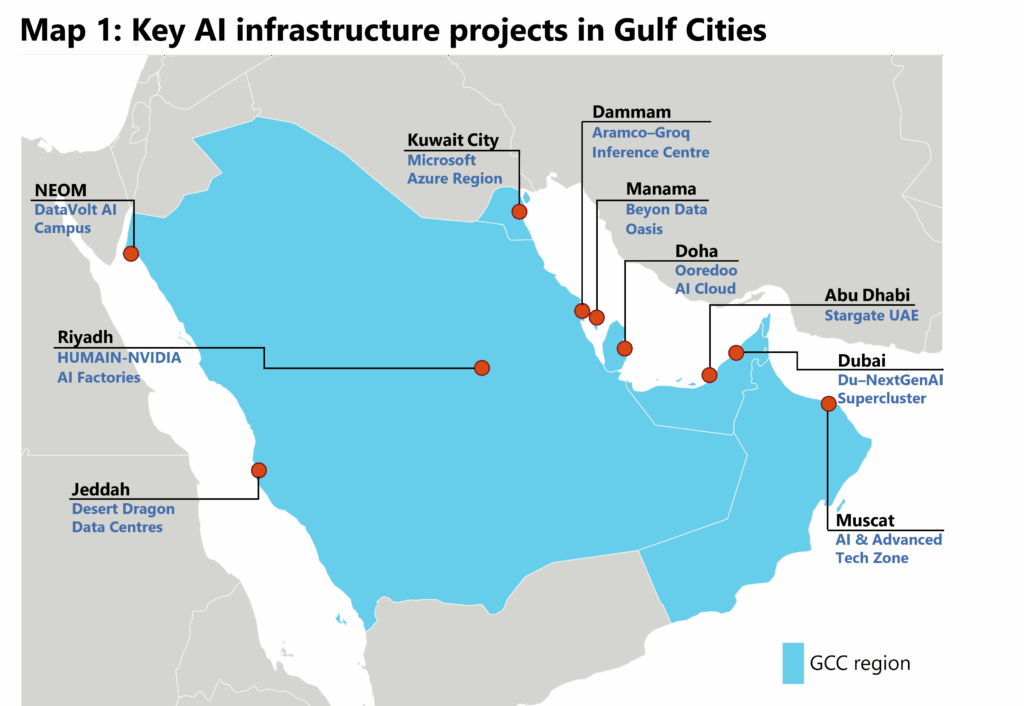

Gulf cities are betting big on AI.

With billions of dollars in planned investment and megawatts of capacity in the pipeline, cities like Riyadh, Abu Dhabi, and Dubai are attempting to position themselves as hubs for AI adoption, infrastructure, and development. The Gulf’s frontrunner cities already score favourably in early adoption, but how well are they positioned to build the data centres, talent, and research ecosystems that power the AI value chain?

As the AI inequality gap becomes ever more relevant, we think that the Gulf’s cities are in a strong position to capitalise on emerging opportunities and strengthen their role in the AI value chain.

Cheap energy meets land availability

AI infrastructure is energy-hungry and space-intensive. In Gulf cities, it finds a natural partner in a geography that keeps power costs low and land plentiful.

In Riyadh and Abu Dhabi, industrial electricity tariffs hover around just $0.05 to $0.07 per kWh—around five to seven times lower than the average UK tariff. Generous energy subsidies and massive new solar farms reinforce this advantage. In Dubai, bids for the 1,800 MW phase of the Mohammed bin Rashid Al Maktoum Solar Park came in at record-lows. Saudi Arabia is moving in the same direction. Al Shuaibah 2, a 2 GW solar project near Jeddah and among the Kingdom’s largest, began commercial operations in 2025, with even more massive installations in the works.

Land is the other geographic boon.

Unlike densely packed tech centres, key Gulf cities are surrounded by open desert, creating room for hyperscale data centres without the land-price pressures that dominate mature hubs. This leaves cities such as Riyadh, Abu Dhabi, and Doha able to plan data centre campuses at scale while staying close to existing utilities and transport links, without running into the sky-high land costs in established tech clusters.

As data-centre power demand rises, questions around local energy prices and grid capacity are growing in urbanised tech hubs like London. We recently forecast that UK data-centre electricity demand could rise fivefold over the next five years. That makes the Gulf’s geography pitch grow even more compelling: cheap energy and ample land that can help deliver AI data centres at a cost base that undercuts traditional hubs in North America and Europe.

Capital, capital, and capital

The AI boom is as much an infrastructure story as a technology one.

Data centres begin with land, permits, and concrete before they ever house the cutting-edge processors that power them. Construction workers, developers, and utilities all sit in the AI value chain, and capital is what keeps it moving.

Gulf capitals just happen to have capital in abundance.

Riyadh and Abu Dhabi are home to massive sovereign wealth funds that have shown readiness to deploy the vast capital necessary to fund domestic AI infrastructure. Hardly a month goes by without news of the region’s active sovereign wealth funds inking infrastructure and AI-related deals. In practice, much of this deployment follows leadership-set mandates, meaning allocations can be more strategic and less price sensitive.

Abu Dhabi’s Mubadala is backing domestic AI champions like the G42 tech conglomerate and seeding new data centre ventures. Riyadh’s PIF has signalled that readiness by launching HUMAIN—a state-backed AI company—and tying it to compute buildouts, including an Nvidia partnership to deploy 18,000 Blackwell chips for a 500 MW AI data centre project.

As this ample financing translates into construction, Gulf cities can offer another advantage. Rapid growth in construction has long been underpinned by relatively low-cost labour. Coupled with strong political will, governments streamlining permitting for priority tech projects can help move infrastructure projects from planning to execution faster and at lower costs.

Addressing the skills gap

While low-cost labour will be instrumental in delivering the infrastructure build out, the Gulf’s cities need to develop and attract the high-skilled labour required to operate, maintain, and scale AI systems in the development phase of the value chain.

Recent upskilling and talent development initiatives aim to address skills gaps. Abu Dhabi launched the first AI-only university (MBZUAI) way back in 2019, and it has now grown to house more than 700 students. In part thanks to this early investment in AI skills, the UAE now ranks first worldwide in AI diffusion according to Microsoft, with 64% of its working-age population using AI by the end of 2025. Qatar also ranks a solid 10th globally. Building on this regional momentum, specialised AI courses are also cropping up. In Saudi Arabia, for instance, established universities such as KFUPM in Dhahran, a city close to Dammam and Bahrain, has introduced new courses focused on AI and machine learning, while the Kingdom has developed a broader suite of major AI training initiatives led by the Saudi Data and AI Authority.

As these programs aim to raise local human capital over time, continued emphasis is being placed on attracting international talent. Immigration policy is being streamlined to bring in expertise faster, with recent expansions to the UAE’s Golden Visa program and Saudi Arabia’s Premium Residency. In cities like Dubai, rapid immigration-driven population growth has coincided with rising office-based employment, consistent with an inflow that is not limited to low-skill labour.

Some limitations remain…

Despite this progress, significant gaps on the skills and innovation front have implications for the Gulf’s readiness to contend in the AI development phase. Much of the most advanced capability still sits upstream in global supply chains, creating export-control exposure. The region doesn’t yet produce cutting-edge semiconductor chips, so major data-centre projects still rely on imported GPUs and international partners to access frontier hardware. That said, the Gulf’s pragmatic links to both Eastern and Western partners widen access to talent and technology.

Additionally, even as the case for the Gulf’s geography strengthens, practical constraints could slow these cities’ ascent as AI hubs. Data centres and AI compute are notoriously water-guzzling ventures, and the Gulf is a water-stressed region. Training and running models generate significant heat, which raises cooling and water demand. The region already relies heavily on desalination to meet water demand, so the cost, scalability, and sustainability of supplying water for large data-centre clusters becomes part of the cost calculus. On the capital front, even as Abu Dhabi launches a dedicated AI investment fund in the form of MGX, the financial muscle of the region’s sovereign wealth funds is being stretched across a wide range of competing priorities.

Even so, we think Gulf cities are well positioned to strengthen their role in the AI value chain. The Gulf’s geography supports hyperscale data centres at a lower operating cost with fewer site constraints than dense established hubs. Combined with deep pools of capital that can fund grid upgrades, permitting, and construction, the region can move from investment intent to live capacity quickly.