Research Briefing

| Mar 3, 2025

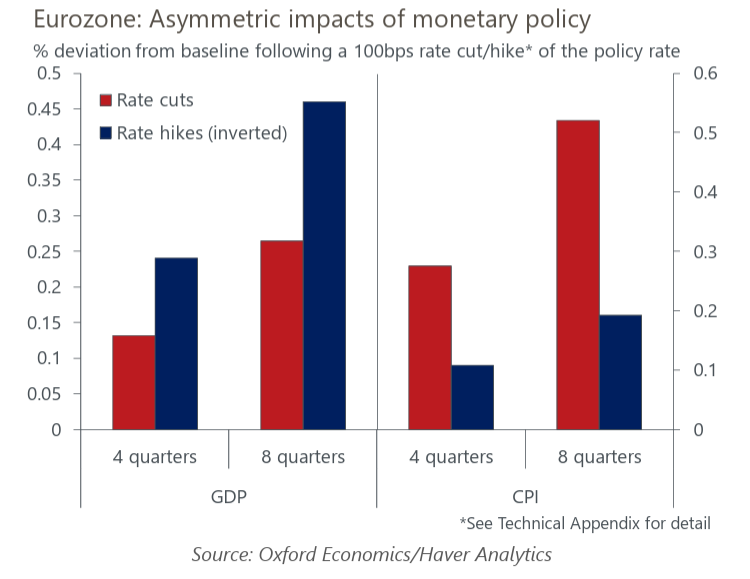

Why rate cuts will do less than rate hikes

Rate cuts by the European Central Bank over the course of 2025 may not boost growth to the same degree that the central bank’s aggressive rate-hiking cycle in the wake of the pandemic constrained it. This reinforces our view that quarterly eurozone growth will remain broadly stable at last year’s humble pace.

What you will learn:

- Our modelling shows rate cuts generate a weaker growth response than rate hikes. But there are also cyclical factors and structural changes to monetary policy transmission in the eurozone that may further dampen the growth boost. Geopolitical and supply-side risks that are keeping term premia elevated will also limit the passthrough of lower nominal rates to financing conditions.

- We also think higher savings since June 2022 won’t be unwound as fast as they were accumulated. Longer maturities on household liabilities mean some of the impact of past rate hikes will likely keep savings elevated. It’s also possible the savings rate could settle higher than the pre-pandemic average. In a post-pandemic era of more adverse supply shocks, consumers are likely to be more risk averse and structurally raise savings over time, dampening the key easing channel of disincentivising savings by lowering rates of return.

- Industrial demand is highly sensitive to interest rates in recessions – rate cuts will provide a much-needed boost. But structural constraints that inhibit profitability, such as labour shortages and higher energy prices, risk subduing investment appetite.

- There may be some upside risks, too. Strong house price growth that bolsters household collateral could deliver a more front-loaded pick-up in durables consumption, which then further supports the beleaguered manufacturing sector.