World Economic Prospects

Each month Oxford Economics’ team of 450 economists updates our baseline forecast for 200 countries using our Global Economic Model, the only fully integrated economic forecasting framework of its kind. Below is a summary of our analysis on the latest economic developments, and headline forecasts. To access the full report (and much more), request a free trial today.

Request a free trial

US and Chinese strength won’t boost all other economies

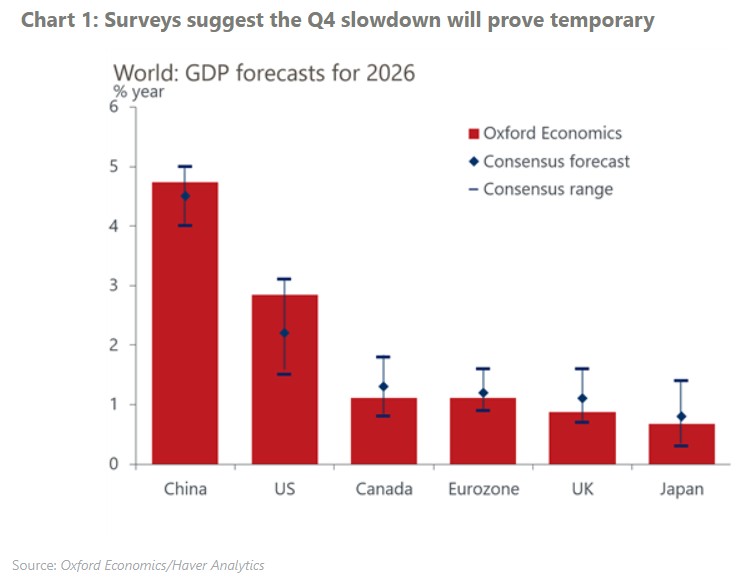

- Upward revisions to US and Chinese GDP growth in Q4 meant that the previously anticipated soft end to 2025 failed to materialise. While we now project activity will rebound by less than we previously expected in early 2026, world GDP growth this year has been mechanically nudged up by 0.1ppt to 3%, in line with last year’s gain.

- The US government shutdown dragged on growth late last year. Still, we estimate the economy recorded a healthy 2.8% q/q annualised gain in Q4 after Q3’s impressive 4.4% rise. Over the coming quarters, the economy is unlikely to match the robust pace of growth recorded in H2 last year. However, we expect overall consumer spending will remain resilient on the back of fiscal stimulus, the recent equity price surge, and a stabilizing labour market. This, along with a broadening of investment away from AI, should ensure that US GDP expands by an above-consensus 2.8% in 2026.

- The Chinese economy grew by 5% in 2025, as activity remained strong in Q4. We anticipate authorities will announce a 4.5%-5% target range for growth in 2026. We’ve raised our GDP growth forecast for China this year by 0.2ppts to an above-consensus 4.7%, positioning it at the midpoint of that range.

- Our above-consensus views on the world’s two largest economies would typically bode well for growth prospects in the rest of the world. However, our forecasts for most other major economies are below the consensus estimates for this year.

- The effects of last year’s tariff increases suggest US import growth will disappoint this year. Furthermore, the persistent effects of geopolitical uncertainty and the ongoing state-driven manufacturing expansion in China will likely dull investment and export prospects. Finally, compared to the US and China, other economies are generally likely to benefit less from fiscal support. The key exception to this trend is APAC – our optimism largely centres on our expectation that the region will continue to benefit from strong AI-related export growth.

Request a Free Trial

Complete the form below and we will contact you to set up your free trial. Please note that trials are only available for qualified users.

We are committed to protecting your right to privacy and ensuring the privacy and security of your personal information. We will not share your personal information with other individuals or organisations without your permission.

Find out how Oxford Economics can help you

Talk to us

Please Add Form