Research Briefing

| Apr 29, 2024

日本央行或将在秋季结束零利率政策

一如预期,日本央行在4月26日的会议上将政策利率维持在 0%-0.1% 的水平。 由于对工资驱动的持续通胀动态更有信心,以及对政策正常化的强烈愿望,日本央行似乎更有可能在秋季结束零利率政策。

你将了解到什么:

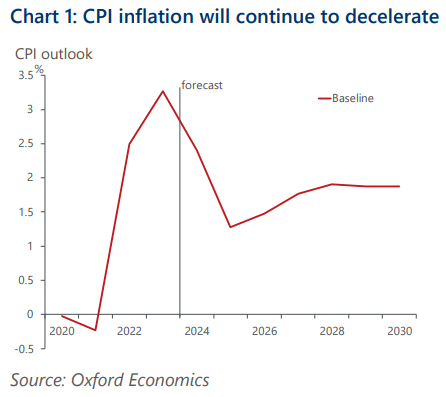

- 《季度展望报告》中对 2024 和 2025 财政年度消费物价指数(不包括新鲜食品和能源)的预测中值保持不变,为 1.9%。 2026 财年的数字为 2.1%,这表明日本央行有信心在未来几年实现 2% 的通胀目标。

- 日本央行越来越强调货币政策取决于数据。 春季谈判中的中小型企业工资解决方案继续带来惊喜。

- 假设实际收入和消费的复苏在夏季得到确认,日本央行很可能会提高其政策利率,理由是实现 2% 目标的可能性已经上升。

- 我们仍然预计日本央行将在 2028 年之前谨慎地将政策利率上调至 1%。 由于中期物价前景存在巨大的下行风险,特别是工资上涨的可持续性和中小企业的定价能力,因此达不到 1%的风险仍然很大。

牛津经济研究院 (Oxford Economics) 是全球领先的独立经济预测及量化分析机构。基于领先的全球经济分析及行业分析模型,我们提供覆盖全球200多个经济体、100多个行业板块和8,000多个城市和地区的经济研究报告、预测及分析工具;并能够协助客户对市场走向进行预测,分析其对于经济、社会及商业的影响,为客户制定决策奠定坚实基础。