Research Briefing

| Mar 7, 2024

工业前景预测亮点:2024年将重塑发展势头

随着 2024 年的到来,全球工业活动应会回升,并开始重建势头。 能源批发价格的下降、过去加息影响高峰期的过去以及去库存周期的低谷都将有利于发达经济体的制造业活动。 按年度计算,我们预计今年的工业增长率为 2.7%。

你将了解到什么:

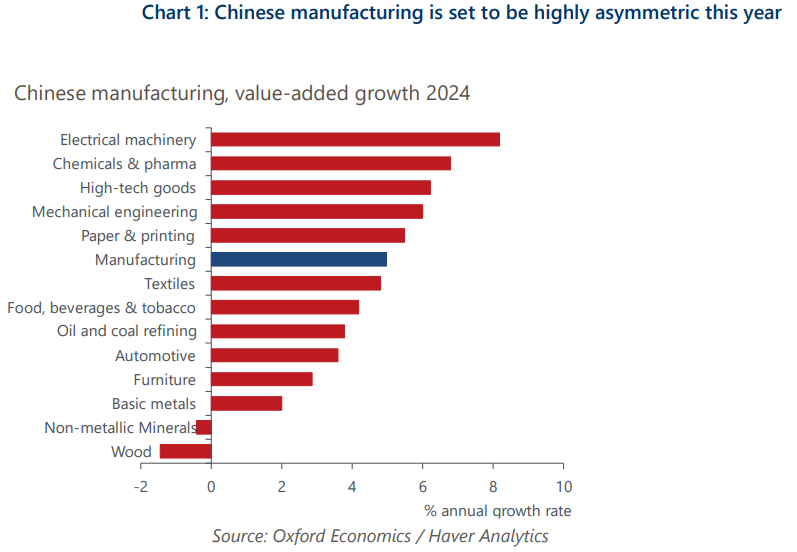

- 在中国,2024 年的增长可能高度不对称,并主要集中在与能源转型相关的“新三样”产业, 以及半导体等高科技产品。 另一方面,房地产行业的持续低迷也将严重阻碍建筑业的发展。

- 战略性产业生产的强劲增长,加上通货紧缩压力和国内需求疲软,意味着中国某些类别商品的出口激增,引发了欧盟政策制定者对中国倾销的指责。

- 欧盟,尤其是德国,是 2023 年全球工业的主要薄弱环节。 虽然短期内经济形势依然不容乐观,但有迹象表明,经济疲软已经触底,到 2024 年,我们应该会看到经济逐步复苏,尽管这种复苏并不明显。

- 胡塞武装对红海航道的袭击对航运活动的干扰预计至少会持续到 2024 年年中。 尽管不确定性很高,但我们认为更广泛的通胀影响应该不大。

牛津经济研究院 (Oxford Economics) 是全球领先的独立经济预测及量化分析机构。基于领先的全球经济分析及行业分析模型,我们提供覆盖全球200多个经济体、100多个行业板块和8,000多个城市和地区的经济研究报告、预测及分析工具;并能够协助客户对市场走向进行预测,分析其对于经济、社会及商业的影响,为客户制定决策奠定坚实基础。